Imagine there is a precise, tactical blueprint in consumer finance that allows you to compare real, personalized borrowing offers from a dozen competing institutions simultaneously, evaluate your true data benchmarks, and finalize a funding arrangement—all without a single point being deducted from your FICO score. To many everyday borrowers under financial stress, this strategy sounds like an impossible workaround. Yet, it represents a standard operational mechanism in the modern banking landscape. This approach is known as soft-pull loan prequalification.

The fact that a vast majority of consumers fail to use this structured method is one of the most expensive errors in personal finance. When faced with an immediate need for capital—whether to manage high-interest credit card debt or fund a home upgrade—most people handle the search backward. They submit multiple formal credit applications across different digital portals out of desperation. This triggers a wave of hard inquiries that can pull down their credit profile just when they need their borrowing power to be at its strongest.

This comprehensive educational manual is designed to pull back the curtain on how prequalification algorithms pull consumer data behind the scenes. We will analyze the strict differences between hard and soft database queries, map out the hidden vulnerabilities inside the FICO model, and provide a clear step-by-step strategy. This guide gives you the tools to shop the credit market confidently, protect your credit score, and ensure your next loan agreement serves your financial goals rather than eroding your household wealth.

The Soft Prequalification Phase

A basic administrative review of your data. Lenders check your credit background and internal credit risk tiers without registering a credit-seeking event on your credit report.

The Hard Formal Application

An official, mandatory credit review submitted to the credit bureaus. It confirms full documentation, stays visible on your credit history for 24 months, and can lower your scores.

Understanding these definitions is the first defensive step in managing consumer credit successfully. Let’s look directly at the credit validation mechanisms to see why mastering this process is essential to protecting your finances.

1. Deconstructing the Mechanics: What Is a Soft Pull and Why Does It Matter?

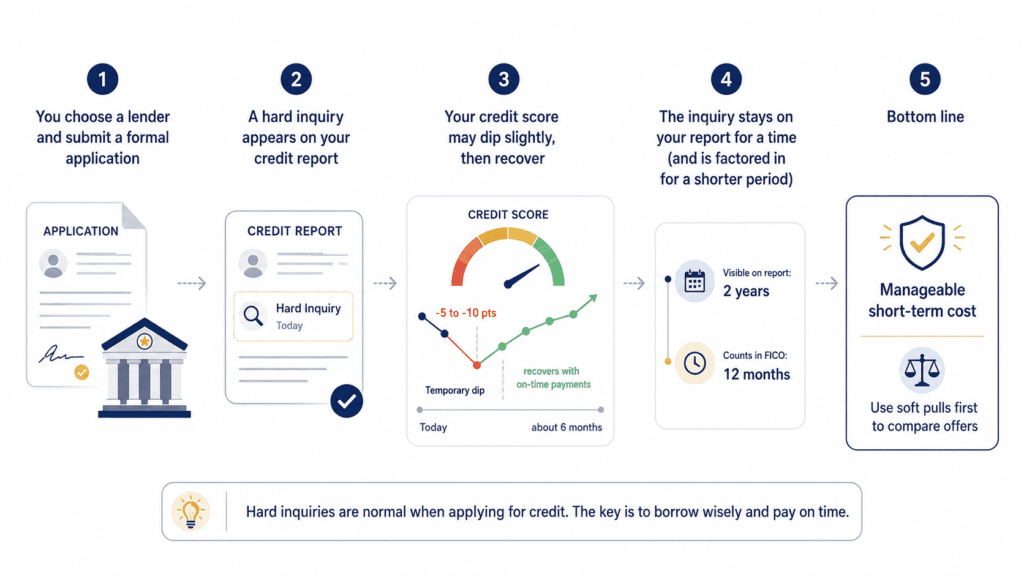

When a lending institution reviews your credit file to assess your reliability as a borrower, they can do so using two completely distinct legal and technological mechanisms: a soft inquiry or a hard inquiry. Failing to recognize the operational differences between these two tracks can have immediate consequences for your financial plans.

The Background Nature of Soft Inquiries

A soft credit check is an administrative query that functions strictly as an information-gathering step. It occurs when a lender reviews your basic credit profile to see if your history matches their standard underwriting tiers. Because a soft pull is not tied to an active, finalized request for a specific line of credit, it is never reported as a credit-seeking event to the primary credit bureaus (Equifax, Experian, and TransUnion).

This means soft inquiries are invisible to other institutions viewing your credit file. They have an absolute **zero point impact** on your active credit scores. In fact, soft pulls occur constantly in the background of your financial life without your direct involvement—such as when a credit card company checks your profile to send a pre-approved offer, or when you pull your own credit report through monitoring platforms to check your history.

The Structural Impact of Hard Inquiries

Conversely, a hard credit check is an official request submitted to the credit bureaus when you complete a formal application for credit. This tells the database that you are actively taking on new financial liabilities. The system logs this entry on your credit file immediately, making it visible to any lender who reviews your background over the next two years.

Because a sudden influx of new debt requests can indicate rising financial risk, the FICO scoring model penalizes your score for each hard check, typically resulting in a temporary drop of **5 to 10 points per inquiry**. If you apply with multiple lenders simultaneously, these individual drops can quickly stack up, creating a significant downward trend across your overall credit profile.

If an unguided borrower formally applies with five different personal loan providers in a short period, they risk a **25 to 50 point drop** on their credit profile. A drop of this size can push an applicant down an entire underwriting tier—shifting them from “Good Credit” to “Fair Credit.” This downward move can result in significantly higher long-term interest rates on the exact financing they are trying to secure.

Before initiating any application process, it is vital to understand where your credit profile sits relative to institutional underwriting boundaries. Reviewing our structural guide on What Credit Score Levels Lenders Demand Across Different Financing Tiers will clarify the exact parameters used to price consumer risk.

2. The Hidden Trap Inside the FICO Personal Loan Algorithm

This section outlines a critical nuance that many everyday borrowers miss: **Personal loan applications do not benefit from the standard rate-shopping protections built into alternative financing markets.**

When you shop around for a mortgage or an auto loan, the architectural code behind the FICO scoring model is designed to be relatively forgiving. The system recognizes that buying real estate or a vehicle requires comparing offers across different lenders. To support this, the algorithm groups multiple mortgage or auto inquiries occurring within a 14 to 45-day window into a **single scoring event**. This approach allows you to cross-reference multiple bank offers without damaging your score.

If you are exploring the housing market this year, understanding these dedicated grouping rules can help you maximize your savings. Review our detailed guide on The Complete U.S. Mortgage Guide to see how to align your property shopping with optimal credit groupings. You can also review our breakdown of Adjustable-Rate vs. Fixed-Rate Mortgages to protect your long-term real estate financing.

However, the personal loan market operates under an entirely different set of rules. **The FICO model does not offer a rate-shopping window for personal installment loans.** Every single formal application you submit to a personal loan provider is treated as an isolated, independent credit-seeking event.

If you submit five formal applications to five different personal loan lenders on the same afternoon, you will trigger five individual hard inquiries, leading to a direct hit to your score. This unique structural rule makes utilizing the soft-pull prequalification framework a necessity rather than an optional optimization tip.

3. Demystifying the Prequalification Engine: How It Works

The soft-pull prequalification framework solves this problem by allowing lenders to build a personalized loan offer without triggering an official hard inquiry on your record. Let’s look closely at how this process works behind the scenes:

1. Soft Data Ingestion

You provide your basic personal identifiers, address, stated gross annual income, and requested loan size. The lender initiates a soft check to view your credit file without creating an official entry on your bureau history.

2. Automated Risk Assessment

The lender’s internal underwriting algorithms check your automated risk metrics, debt-to-income balance, and payment history against their specific credit tiers to determine eligibility.

3. The Conditional Offer Payout

If your profile satisfies their criteria, the platform generates a real, personalized offer detailing your projected APR, approved loan amount, and repayment term options—all with zero impact on your credit score.

It is important to understand that a prequalification offer is not an absolute, binding guarantee of final loan approval. Instead, it functions as a highly accurate, conditional preview. The final terms are confirmed during the subsequent formal stage, where the lender runs a hard credit check to verify your full documentation, employment records, and identity information.

To ensure your initial automated prequalification offers turn into smooth final approvals, optimizing your credit health ahead of time is key. Take time to read our master manual on How to Improve Your Credit Score Before Applying for a Mortgage or Personal Financing to position your profile for the most competitive pricing tiers available.

4. The 2026 Reference Guide: Major Soft-Pull Lenders

The modern personal lending market is divided between automated fintech platforms that utilize soft-pull frameworks for initial rate quotes and traditional commercial banks that may require an immediate formal application.

The matrix below outlines the fee structures, prequalification paths, and upper-tier APR caps across major providers:

| Lending Institution | Soft-Pull Available? | Hard Inquiry Trigger Point | Origination Fee Scale | Maximum Advertised APR |

|---|---|---|---|---|

| SoFi | Yes | Upon formal application submission | 0.00% (Fee-Free Model) | 29.99% APR |

| Marcus (Goldman Sachs) | Yes | Upon formal application submission | 0.00% (Fee-Free Model) | 24.99% APR |

| Discover | Yes | Upon formal application submission | 0.00% (Fee-Free Model) | 24.99% APR |

| LendingClub | Yes | Upon formal application submission | 1.00% – 8.00% | 35.99% APR |

| Upgrade | Yes | Upon formal application submission | 1.85% – 9.99% | 35.99% APR |

| Upstart | Yes | Upon formal application submission | 0.00% – 12.00% | 35.99% APR |

| Best Egg | Yes | Upon formal application submission | 0.99% – 9.99% | 35.99% APR |

| LightStream | No | Triggers hard pull immediately at entry | 0.00% (Fee-Free Model) | 25.49% APR |

| Credible (Marketplace) | Yes (One Pull) | Bypassed until committing to one lender | Varies by partner lender | Varies by partner lender |

| MoneyLion (Marketplace) | Yes (One Pull) | Bypassed until committing to one lender | Varies by partner lender | Varies by partner lender |

This matrix illustrates that while most prominent digital platforms leverage soft pulls to protect your credit profile during the initial shopping phase, outliers like LightStream bypass prequalification entirely and run a hard check immediately. This makes careful review of each platform’s terms essential.

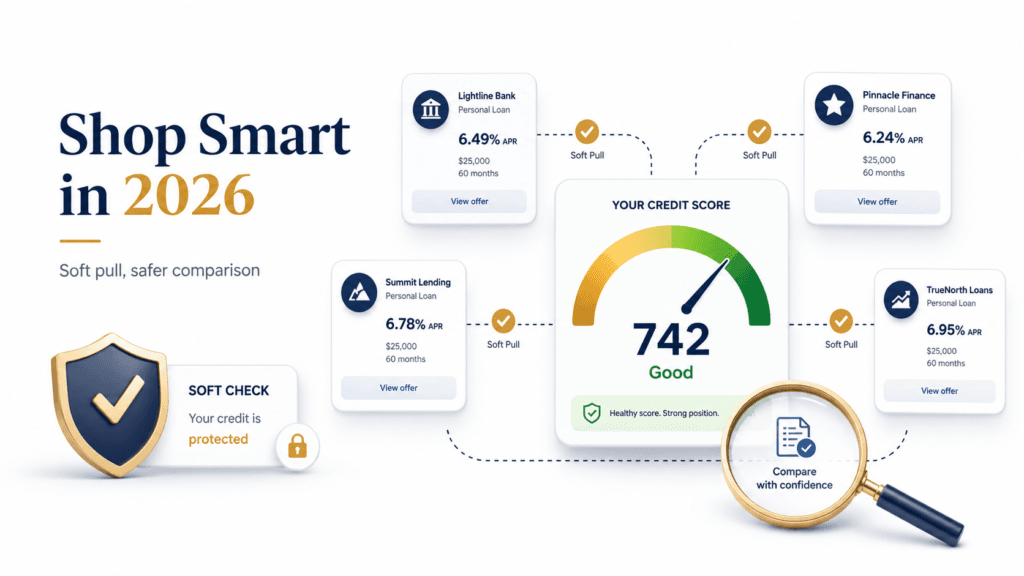

5. The Marketplace Shortcut: Aggregating Offers via a Single Soft Pull

If visiting individual lender websites and entering your personal data multiple times feels like too much friction, the consumer lending market provides an efficient shortcut: **loan comparison marketplaces**.

Platforms like Credible, MoneyLion, and similar fintech aggregators act as centralized communication hubs between consumers and a broad network of partner banks. Instead of submitting individual requests, you fill out a single prequalification profile detailing your stated gross income, employment status, housing costs, and target loan size.

The marketplace pushes that single data profile through a secure application interface to dozens of distinct underwriters simultaneously, performing **one collective soft credit pull**. Within minutes, your dashboard fills with real, prequalified offers tailored to your exact history. Every option displays its accompanying APR, origination adjustments, monthly payment obligations, and loan terms side-by-side.

This panoramic method is incredibly valuable if you aren’t sure which platforms are likely to approve your background, or if you simply want to check multiple options quickly before narrowing your focus to a single lender.

Marketplace prequalification tools are highly effective when consolidating short-term debts into a structured repayment plan. If you are balancing multiple revolving lines and looking to minimize your total borrowing costs, read our comprehensive guide on Personal Loans vs. Credit Cards: Which Option Saves More Money? to choose the optimal financial vehicle for your plan.

6. The Verification Protocol: Spotting Deceptive Lender Jargon

As you navigate different financial platforms, you must learn to recognize that not every digital lending page uses consumer lending terms in the exact same way. Some alternative lenders use the word “prequalification” or “pre-approval” on their marketing banners as a psychological hook, while burying a hard inquiry authorization within their consent agreements.

To defend your credit profile against these hidden checks, use this strict verification protocol before clicking any submission button:

- Analyze the Core Disclosure Text: Look for explicit legal text positioned near the submission box. If the page states “Checking your customized rates will not affect your credit score,” or “We utilize a soft inquiry to verify your options,” you are on a safe prequalification track.

- Spot the Hard Pull Warning Signs: If the fine print reads “By clicking submit, you authorize this institution to obtain a full consumer credit report from Equifax/Experian,” or if the system requires you to upload formal income verification documents (like W-2 forms or pay stubs) during the initial step, you are likely triggering a formal hard check. Step back and look for a alternative platform.

If you encounter platforms that obscure their true verification steps, treat that lack of transparency as a clear indicator of how they handle business. Move toward transparent institutions that respect your credit health.

7. The Step-by-Step Strategic Action Plan

To find the most competitive loan terms on the market while keeping your credit score completely secure, execute this clear three-phase strategy:

Phase 1: Broad Prequalification Shopping

Dedicate a single afternoon to collecting initial rate quotes. Visit either a centralized loan comparison marketplace or individual soft-pull lender websites (like SoFi, Discover, or Marcus) and complete their prequalification profiles. Limit your scope to four to six transparent platforms. This step takes less than thirty minutes, keeps your credit file safe, and generates a collection of real, personalized financing offers.

Phase 2: Total Cost Analysis

Look past the initial interest rates and evaluate each offer using the **Annual Percentage Rate (APR)**. The APR accounts for both the base interest and any front-loaded origination fees, providing an accurate look at your true long-term expenses.

If you are exploring different ways to clear existing balances, remember that a lower interest rate paired with an expensive origination fee might not be your most cost-effective path if you plan to pay off the debt early. Review our educational guide on Pay Off Debt vs. Invest: The Mathematical Formula to Guide Your Cash Allocation to align your repayment timeline with your broader financial goals.

Phase 3: Focused Formal Application

Once you isolate the single offer that delivers the lowest true APR and the most comfortable repayment terms, move forward with that specific institution. Submit your formal application and provide your income documentation. This step will trigger a single hard inquiry, resulting in a minor, temporary 5 to 10-point drop on your report—a manageable and short-lived cost for securing the most competitive rate available on the market.

8. The Aftermath: What Happens After the Hard Pull?

Once you finalize your choice and authorize the formal application, the resulting hard inquiry will appear on your bureau files. While hard checks remain visible on your credit history for a full 24 months, their influence on your active credit scores typically disappears after **12 months**.

In most cases, that minor drop is completely recovered within six months of consistent, on-time payment behavior. As you steadily reduce the loan principal, you also improve your credit utilization metrics and add positive history to your payment record, strengthening your credit file for future financial milestones.

Securing a competitive interest rate is an excellent step, but true financial peace of mind requires a sustainable repayment strategy. Taking the time to study our educational guides on How to Build a Budget That Actually Works will ensure your new financing integrates smoothly into your monthly household cash flow.

Ultimately, the soft-pull prequalification framework is not a loophole or a temporary workaround. It is a structured consumer protection system working exactly as intended: giving you the clear data you need to make an informed financial choice before committing your hard-earned capital. By shopping smart, protecting your credit score, and comparing total costs accurately, you can safely navigate the credit market and keep your financial future secure.

Optimize and Protect Your Credit Profile

Do not let hidden transaction fees or unoptimized applications slow your financial progress. Explore our core educational manuals to strengthen your credit metrics, manage debt efficiently, and maximize your cash flow this year:

- The Underwriting Masterclass: How to Optimize Your Scores Before Applying

- Personal Loans vs. Credit Cards: Which Option Costs More in 2026?

- Understanding Debt-to-Income Metrics: What Underwriters Actually Evaluate

- The Cash Flow Engine: How to Design a Sustainable Monthly Budget Plan

- Consumer Financial Protection Bureau (CFPB). What is a Credit Inquiry and How Do Soft vs. Hard Pulls Affect Consumers?

- FICO Credit Scoring Amortization Guidelines. Evaluating Rate-Shopping Grouping Differences Across Residential, Auto, and Installment Financing.

- National Credit Union Administration (NCUA). Consumer Protection Frameworks and Lending Rate Ceilings.