Most Americans spend more time choosing a restaurant than reading a personal loan agreement. That asymmetry can cost thousands. The interest rate on the front page of the offer is only one number inside a document built to protect the lender — and nine of its clauses deserve your full attention before you sign.

Key Takeaways

- Under the Truth in Lending Act (TILA), lenders must disclose all fees and terms — but disclosing them is not the same as making them obvious

- The origination fee, prepayment penalty, and penalty rate trigger are the three clauses with the highest average dollar impact on U.S. borrowers

- A single missed payment can trigger a permanent rate increase on the remaining loan term — far more costly than the late fee itself

- Mandatory arbitration clauses — present in many lender agreements — waive your right to a jury trial and class action participation

- All of these clauses are legal and enforceable under U.S. law. The only protection is reading and understanding them before you sign

Why This MattersThe Gap Between the Offer and the Agreement

A personal loan offer is marketing. The loan agreement is a contract. These are not the same document, and they do not always tell the same story. The offer shows you the rate, the monthly payment, and the term. The agreement contains the conditions under which that rate can change, the fees that apply when things go wrong, and the rights you surrender by signing.

The Truth in Lending Act (TILA) and its implementing regulation, Regulation Z, require lenders to disclose APR, finance charges, and total payment amounts clearly. The CFPB enforces these rules. But legal disclosure is not the same as clarity — and the nine clauses below are consistently the ones that catch borrowers off guard after the fact, not before.

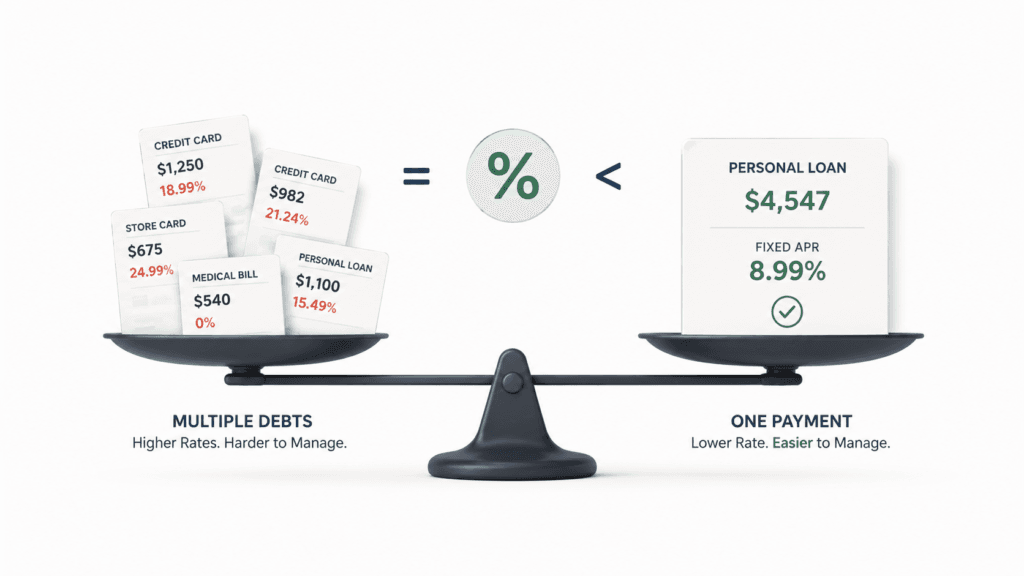

Before exploring what’s buried in the fine print, it helps to understand the full cost picture of personal borrowing. Our analysis of personal loans vs. credit cards: which costs more in 2026 covers how these instruments compare across different balance sizes and repayment scenarios.

The 9 ClausesWhat to Read, What to Ask, and What It Can Cost You

Origination fees range from 1% to 8% of the loan amount and are deducted before you receive a single dollar. On a $15,000 loan with a 6% origination fee, you receive $14,100 but owe $15,000 from day one — and you pay interest on the full $15,000 for the life of the loan. The fee is included in the APR calculation as required by TILA, but many borrowers focus on the interest rate and miss the origination charge entirely.

Many credit unions and online lenders offer zero origination fees for qualified borrowers. If your lender charges one, the question to ask is: “What is the exact net amount I will receive after all fees?” If that number doesn’t cover your full payoff target, you need to borrow more or find a different lender.

Unlike mortgages — where the Dodd-Frank Act heavily restricts prepayment penalties — personal loans carry no equivalent federal protection. Some lenders charge 1%–5% of the remaining balance, or the equivalent of 60–90 days of interest, if you pay off the loan early. This directly punishes the financially responsible behavior of paying ahead.

This must be disclosed under TILA but is easy to miss. Many top-tier lenders charge no prepayment penalty at all — make this a non-negotiable screening question before accepting any offer.

This is the most financially dangerous clause most borrowers never notice. The late fee — typically $15–$40 — is visible and obvious. The penalty rate trigger sits separately, often deep in the default provisions. A single payment that falls 30 days late can permanently increase your rate from, say, 12% to 24% for the remaining loan term.

On a $15,000 loan at 12% APR with 4 years remaining, a permanent rate increase to 24% adds approximately $3,600 in additional interest. Set up autopay with a dedicated account buffer and build the emergency fund that prevents a short income disruption from triggering a permanent rate penalty.

Autopay discounts of 0.25%–0.50% are widely advertised by personal loan lenders. What the advertisement doesn’t say: a single failed autopay — from an account with insufficient funds — can permanently remove that discount for the entire remaining loan term. Some lenders also charge a returned payment fee of $25–$35 on top.

Never link autopay to an account that could run low. A dedicated account holding a permanent reserve of at least two loan payments eliminates this risk entirely. Understanding how to build a budget that accounts for fixed debt obligations is the underlying discipline that makes this manageable.

This clause is standard in virtually every U.S. personal loan agreement. When triggered — typically after two or three missed payments — it converts a manageable delinquency into an immediate demand for the entire remaining balance. A borrower who owes $9,000 on a personal loan suddenly owes $9,000 right now, not in monthly installments.

Failure to pay an accelerated balance leads to charge-off, collections, potential lawsuit, and in some states, wage garnishment. This clause is non-negotiable — it exists in every contract. The only protection is the financial buffer that prevents you from ever reaching the trigger point. Our complete guide covers exactly how much emergency fund you need and how to build it alongside debt repayment.

This clause eliminates your right to sue the lender in court and your right to join a class action lawsuit. The CFPB has documented extensively that arbitration awards to consumers are consistently lower than court judgments, and that class action lawsuits have historically recovered hundreds of millions of dollars in improperly charged fees that individual arbitration never would have surfaced.

You cannot negotiate this clause away at most major lenders. Your best option is to choose a lender — often a federal credit union or community bank — whose agreements do not include mandatory arbitration. Search the full agreement for the words “arbitration,” “jury waiver,” and “class action.”

Personal loans are most commonly fixed-rate — but not always. Some lenders, particularly those offering lower introductory rates, tie the rate to a benchmark like the Secured Overnight Financing Rate (SOFR) — which replaced LIBOR as the U.S. benchmark rate. A loan starting at 10.5% APR could become 13.5% or higher if the benchmark moves. The word “fixed” in marketing materials does not guarantee a fixed rate in the actual contract.

For context on why rate certainty matters, consider how this same risk affects mortgage borrowers — our guide to fixed vs. adjustable rate mortgages explains the tradeoffs in depth. The same logic applies to any installment debt in an uncertain rate environment.

This clause is common at banks and credit unions where borrowers hold multiple products. If you have a checking account, auto loan, credit card, or savings account at the same institution, a default on any one of them — an overdraft, a missed car payment, a triggered credit card penalty — can legally constitute a default on your personal loan, even if you have never missed a single personal loan payment.

If you are at risk on any other obligation at a financial institution, consider borrowing your personal loan from a different lender. This is especially relevant for borrowers managing multiple debts simultaneously — our DTI guide helps you see your full exposure before taking on any new obligation.

Credit life insurance, disability insurance, and “payment protection plans” are optional products that some lenders bundle into the loan payment — often without clear verbal disclosure during the application process. The FTC’s Credit Practices Rule requires these to be optional, not automatic. In practice, they appear as a line item in the monthly payment that many borrowers never question.

Check your loan documentation for terms like “payment protection,” “credit life,” “accident and disability coverage,” or “involuntary unemployment protection.” If you did not specifically request it, ask for it to be removed. Most lenders will do so without issue — but only if you ask.

Before You SignSeven Questions to Ask Any Lender in Writing

Reading a full loan agreement before signing is the right thing to do — and still leaves room for things to be misunderstood. These seven questions, asked in writing and answered in writing, give you a clear record of what you agreed to:

- What is the net amount I will actually receive after all fees, including the origination fee?

- Is there a prepayment penalty? If so, what is the formula and when does it apply?

- Is the interest rate fixed for the entire loan term, regardless of any benchmark rate changes?

- Does a late payment trigger a permanent rate increase? If so, what is the threshold and the new rate?

- Does the loan agreement include a mandatory arbitration clause?

- Does a default on any other product at this institution constitute a default on this loan?

- Are any insurance or protection products included in the monthly payment? If so, what are they and how do I remove them?

A lender unwilling to answer these questions directly and in writing is telling you something important. The CFPB’s personal loan resource center provides free guidance on your rights as a borrower and what disclosures are legally required before any loan closes.

Once you understand what a loan truly costs, the decision of whether to borrow — and from whom — becomes much clearer. If your goal is debt consolidation, our guide on eliminating credit card debt in 2026 covers the full range of strategies, including when a personal loan is the right tool and when it isn’t. And if you are trying to understand how any new loan affects your borrowing capacity for a future mortgage or major purchase, our DTI ratio guide walks through the calculation lenders use to evaluate your entire debt picture.

Sources & References

- Consumer Financial Protection Bureau (CFPB) — Personal Loans: What You Need to Know. consumerfinance.gov

- Consumer Financial Protection Bureau — Regulation Z (Truth in Lending) — 12 CFR Part 1026. consumerfinance.gov

- Consumer Financial Protection Bureau — Arbitration Study: Report to Congress, 2015. consumerfinance.gov

- Federal Trade Commission — Credit Practices Rule: Consumer Credit Regulations. ftc.gov

- Federal Reserve — Consumer Credit — G.19 Statistical Release, 2026. federalreserve.gov

- Dodd-Frank Wall Street Reform and Consumer Protection Act — Title XIV: Mortgage Reform and Anti-Predatory Lending Act, 2010. congress.gov

- Bankrate — Personal Loan Fees Survey: Origination Fees and Prepayment Penalties, 2026. bankrate.com

- Experian — What Is an Acceleration Clause in a Loan Agreement? experian.com