Every business owner eventually faces the same moment: the company needs capital, and the bank says no — or says yes, but with conditions buried in fine print that no one fully explained. Business financing, whether in the United States or the European Union, is one of the most consequential decisions a company’s leadership will ever make. Done right, it fuels growth, stabilizes cash flow, and builds long-term equity. Done wrong — or done in desperation — it can destroy in eighteen months what took ten years to build.

This is the story of business financing told honestly: the legitimate paths, the predatory shortcuts, the clauses that lenders don’t volunteer, and — critically — what happens when a company stops paying and how it can recover.

The Financing Landscape: Why Geography Shapes Everything

Before comparing individual products, one structural fact defines everything else: bank loans make up around 70% of external financing for SMEs in Europe, compared to roughly 40% in the United States. This single statistic explains why American and European businesses face fundamentally different financing realities, risk profiles, and vulnerability to predatory products.

In the US, the capital markets ecosystem is deep, diverse, and — for better or worse — largely unregulated in its alternative segments. In Europe, businesses depend heavily on a more conservative banking system, supported by a robust framework of public and EU-backed programs — but constrained by collateral requirements and bureaucratic timelines that leave many SMEs chronically underfinanced.

PART ONE: Business Financing in the United States

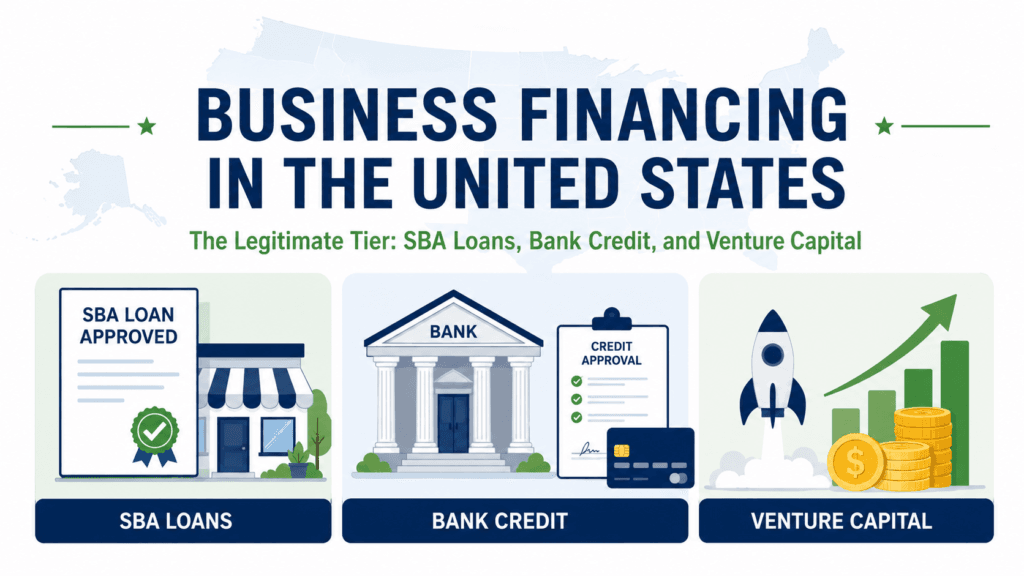

The Legitimate Tier: SBA Loans, Bank Credit, and Venture Capital

The gold standard of American small business financing is the SBA loan — a government-backed product administered through approved private lenders. SBA-guaranteed loans generally have rates and fees comparable to non-guaranteed loans, with lower down payments, flexible overhead requirements, and no collateral needed for some loans. Expatica

The flagship program, the SBA 7(a) loan, is the most widely used. Most 7(a) loans have a maximum loan amount of $5 million. The SBA guarantees up to 85% of loans of $150,000 or less, and up to 75% of loans above $150,000. Repayment terms vary from 7 to 25 years, depending on the use of funds. SBA 7(a) rates are based on either the prime rate or the SBA’s optional peg rate — currently 4.50% for Q1 2026 — plus a spread. For businesses that qualify, this is genuinely competitive financing.

For real estate and major equipment, the SBA 504 loan goes further. SBA 504 loans typically fall within a 5% to 7% effective rate range, are fixed for the life of the loan, and require a down payment of at least 10%. A traditional lender puts up 50% of the loan, and a certified development company (CDC) puts up as much as 40%.

At the smallest scale, the SBA Microloan Program provides up to $50,000. Interest rates for SBA microloans generally fall between 8% and 13%, with repayment terms of up to seven years. It is one of the most accessible entry points for startups, underserved entrepreneurs, and businesses without traditional collateral. Hypoteky

Beyond SBA programs, conventional bank lending, venture capital, angel investment, and revenue-based financing round out the legitimate US business financing ecosystem. Invoice factoring — selling outstanding receivables at a discount to unlock immediate cash — is also widely used and legitimate when terms are clearly disclosed.

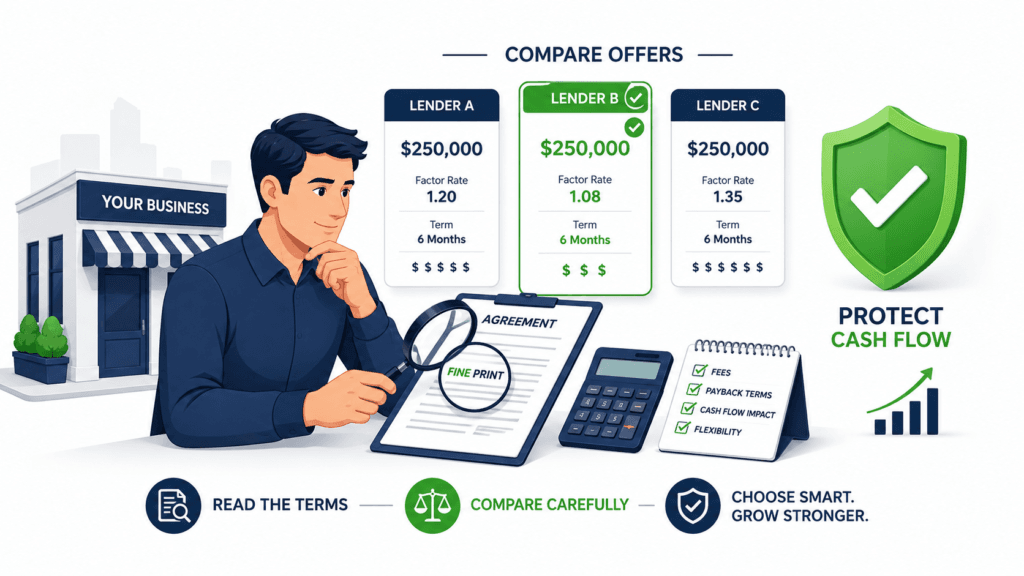

The Shadow Tier: Merchant Cash Advances and the Debt Trap Nobody Warns You About

Here is what many business financing brokers and alternative lenders will not put in their pitch decks.

A merchant cash advance (MCA) is often compared to a payday loan for a business. It is technically not a loan but a purchase of a company’s future sales. The lender gives money upfront and then takes a weekly or daily cut of receipts directly from the borrower’s bank account until the debt is repaid — and then some. The lender does not need to be licensed, the fees have no legal cap, and because the debt is usually due within months, the equivalent annual interest rate can be astronomical. European Central Bank

The numbers are not abstract. Merchant cash advances carry factor rates that translate to effective APRs of 100% to 400%, combined with daily repayment structures that drain cash flow and hidden fees buried in complex agreements.

The MCA industry has grown dramatically in recent years — accelerated, notably, by tariff-driven cost shocks. As tariffs drove up costs for many businesses in 2025, many firms turned to merchant cash advances to stay afloat. According to Democratic Senators Ed Markey and Ron Wyden, the SBA changed a rule that previously allowed MCA-trapped businesses to refinance into government-backed loans — effectively closing an essential escape route for small businesses spiraling in MCA debt. The senators described the effective APRs on these products as regularly exceeding 100%.

The legal architecture that makes MCAs dangerous is deliberate. MCA agreements are structured as purchases of future receivables, which allows lenders to bypass state usury laws that cap interest rates. Many MCA contracts violate the spirit of usury laws by charging outrageous rates disguised as “fees,” and some include Confession of Judgment (COJ) clauses — provisions that allow the lender to obtain a court judgment against the business without prior notice. Many MCA contracts allow the provider to file collection suits in their own local courts, not the courts of the business being sued — a geographic tactic that makes litigation prohibitively expensive for the borrower. European Central BankTRADING ECONOMICS

The SBA itself warns business owners to watch out for interest rates significantly higher than competitors’ rates, fees more than 5% of the loan value, and any lender who asks you to lie on paperwork or leave signature boxes blank.

PART TWO: Business Financing in the European Union

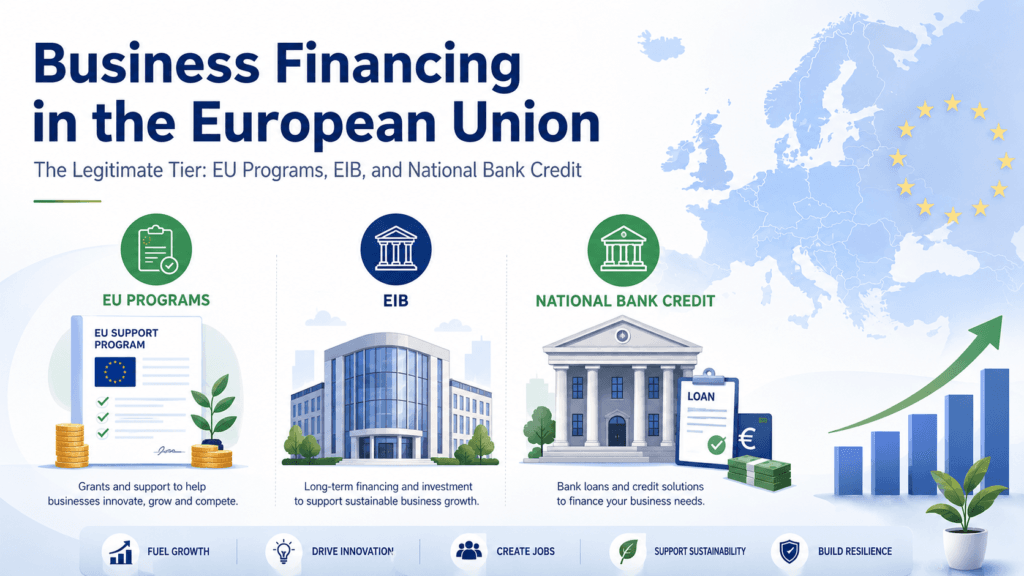

The Legitimate Tier: EU Programs, EIB, and National Bank Credit

European SMEs operate within a layered financing ecosystem that combines national banking systems with an extensive framework of EU-backed programs. The depth of this public support infrastructure is genuinely superior to what exists in the United States — but accessing it requires navigating bureaucracy that smaller businesses frequently lack the resources to manage.

The cornerstone programs are:

InvestEU / COSME: The InvestEU programme aims to trigger €372 billion in new investment using an EU budget guarantee. Under the SME window, it supports businesses perceived as high-risk or with insufficient collateral, including innovative businesses and those adopting digital practices. The earlier COSME program supported over 800,000 SMEs with more than €50 billion in financial debt support. COSME provides loan guarantees of up to €150,000 for SMEs, while the EaSI program provides microloans of up to €25,000 for micro-enterprises. Mortgage MarkFannie Mae

European Investment Bank (EIB): The EIB lends to SMEs indirectly through local financial institutions, providing below-market funding lines that participating banks can then pass through to businesses. This channel produces some of the most favorable rates available to European businesses — but requires an established relationship with a participating bank.

Horizon Europe: For innovative or R&D-oriented businesses, Horizon Europe grants represent non-dilutive, non-repayable capital — the most cost-effective financing possible. The application process is demanding, but for qualifying companies, this funding carries no repayment obligation.

Across most EU member states, the primary route to business credit remains the traditional bank loan, supplemented by these EU guarantee and grant mechanisms. Interest rates for SME loans in the eurozone currently track near the ECB’s main refinancing rate of 2.15%, though spreads and risk premiums push the effective borrowing cost higher for less-established businesses.

The Hidden Risks in European Business Financing

The EU’s regulatory framework is more protective of business borrowers than the American system in several respects — but it is not without its own predatory corners.

Information asymmetries significantly hamper SMEs’ borrowing capacity. Financially troubled businesses find it more difficult to secure outside funding than financially sound businesses, which creates a dangerous dynamic: the businesses that most need capital are the ones most likely to be pushed toward more expensive, less transparent products.

In practice, this means that European SMEs rejected by traditional banks frequently turn to private lenders, factoring companies, and alternative finance platforms operating under varying national regulatory frameworks. Unlike the US, where the CFPB at least attempts to standardize disclosure requirements, the EU’s patchwork of national implementations of the Late Payments Directive and the Commercial Credit Directive leaves meaningful gaps. Loan terms, prepayment penalties, and variable rate clauses vary dramatically across France, Germany, Spain, and Italy — and lenders are under no uniform obligation to disclose the effective APR in the same way consumer lenders must.

Cross-border business lending adds another layer of complexity. A Spanish SME taking a loan from a Dutch alternative lender — a transaction entirely legal within the single market — may find that the governing jurisdiction for disputes is Amsterdam, not Madrid, and that the legal costs of challenging abusive clauses in a foreign court are effectively prohibitive.

When the Company Can’t Pay: What Actually Happens

This is the part of the story that financing brokers never tell prospective clients.

In the United States, a business defaulting on an SBA loan faces a structured resolution process. The SBA will typically attempt a negotiated settlement before initiating legal action, and personal guarantees — which SBA loans almost always require from owners with 20% or more equity — mean that the business’s failure can become the owner’s personal financial crisis. Assets pledged as collateral will be liquidated. Credit histories, both business and personal, will be damaged for years.

For MCA defaults, the process is faster and more brutal. If a business misses a payment or falls behind on its MCA repayment schedule, it may be subject to penalties, increased fees, and legal action. The aggressive repayment terms of some providers create more problems than the original cash flow issue they were meant to solve. A COJ clause can result in a bank account freeze within days.

In the European Union, default procedures vary by country. French and German insolvency frameworks offer restructuring options that are generally more favorable to the debtor than their US equivalents. Spain’s recent insolvency law reforms have improved restructuring flexibility for SMEs significantly. However, businesses in Southern Europe — particularly those with personal guarantees on bank loans — face the same personal asset exposure as their American counterparts.

The Recovery Path

The single most important action a business can take when it realizes it cannot meet its financing obligations is to act before the default, not after. Both in the US and the EU, lenders have significantly more flexibility — and significantly more incentive to negotiate — before a loan enters formal default status.

In the US, SBA-backed lenders are required to exhaust reasonable workout options before triggering guarantee claims. An attorney specializing in business debt restructuring can often negotiate extended repayment terms, principal reductions, or formal settlement agreements that avoid the most damaging consequences of outright default.

In Europe, the combination of national insolvency frameworks and EU Directive 2019/1023 on preventive restructuring frameworks gives distressed businesses legal tools to impose restructuring plans on dissenting creditors — a powerful mechanism that few SME owners know exists or know how to invoke.

The fundamental lesson on both sides of the Atlantic is this: business financing is a tool that becomes a weapon when misunderstood or misused. The companies that survive financial distress are almost always those that understood the terms before they signed — and sought legal counsel before the situation became irreversible.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Information about loan programs, rates, and regulatory frameworks is based on publicly available sources as of May 2026 and is subject to change. Laws and programs vary significantly by country, state, and jurisdiction. Always consult a licensed financial advisor and qualified legal counsel before entering into any business financing agreement.

Sources

- U.S. Small Business Administration. (2026). Loans — SBA 7(a) Program, 504 Program, and Microloans. sba.gov

- NerdWallet. (May 2026). SBA Loan Rates May 2026. nerdwallet.com

- Nav. (March 2026). SBA Loan Requirements: Complete Guide to Qualifying in 2026. nav.com

- Clarify Capital. (April 2026). SBA Loan Requirements 2026 and Current SBA Loan Rates Explained. clarifycapital.com

- American Banker. (May 15, 2026). Democrats Say SBA Left Businesses Vulnerable to Predatory Financing. americanbanker.com

- NPR. (February 2026). A Shadowy Industry Is Helping Small Businesses Pay Tariffs — At a High Cost. npr.org

- Crestmont Capital. (March 2026). Common Business Loan Scams and How to Avoid Them. crestmontcapital.com

- J. Singer Law Group. (February 2026). Merchant Cash Advance Lawsuit: How to Protect Your Business and Legal Rights. singerlawgroup.com

- Davis Business Law. (February 2025). Merchant Cash Advance: Fast Funding for Small Businesses — But Beware the Legal Perils. davisbusinesslaw.com

- European Commission. (2026). Funding Opportunities for Small Businesses. commission.europa.eu

- European Commission. (2026). EU-Supported Loans, Guarantees and Equity Investments. single-market-economy.ec.europa.eu

- EUcalls. (January 2026). European Funding for Small Businesses. eucalls.net

- Allianz Trade. European Regulatory Changes Will Make Banks Less Willing to Lend to SMEs. allianz-trade.com

- Journal of Small Business Strategy. (June 2025). SMEs’ Access to Bank Financing During the Financial Crises in Europe. jsbs.scholasticahq.com

- European Parliament. (2019). Directive 2019/1023 on Preventive Restructuring Frameworks. europarl.europa.eu