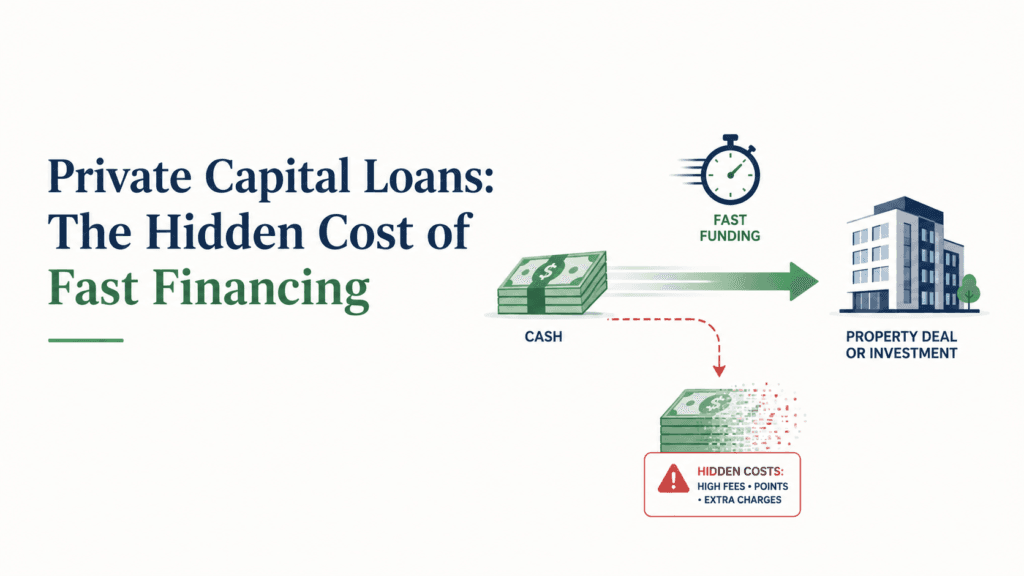

When traditional banks say “no,” private capital lenders often step in with a tempting promise: fast approval, flexible terms, and money in your account within days. For many borrowers—especially small business owners, freelancers, or individuals with imperfect credit—this seems like salvation. But in 2026, as interest rates remain high and credit standards tighten, these private loans are increasingly becoming a financial trap rather than a lifeline.

This article examines how private capital loans work, why they can turn into a long‑term problem, and what real solutions exist for borrowers in both the United States and the European Union.

1. The Appeal of Private Capital Loans

Private capital loans—often called hard money loans in the U.S. or private financing in the EU—are typically funded by individuals, investment groups, or non‑bank institutions. They are marketed as fast, flexible, and accessible for borrowers who fail to meet bank criteria.

Why people choose them

- Speed: Approval can take 24–72 hours, compared to weeks for a bank loan.

- Less paperwork: Minimal documentation and no long credit history required.

- Collateral‑based: Approval often depends on asset value (property, vehicle, or business equipment) rather than credit score.

- Short‑term use: Ideal for bridging finance, property flips, or emergency liquidity.

In theory, these loans fill a gap left by traditional banking. In practice, they often shift risk from the lender to the borrower, with little regulatory oversight.

2. The Hidden Costs Behind “Fast Money”

High interest rates

According to the U.S. Federal Reserve’s 2025 lending data, private capital loans average between 12% and 30% APR, compared to 6–8% for conventional bank loans. In the EU, the European Banking Authority reports similar figures, with private lenders charging 10–25% APR depending on country and collateral.

Fees and penalties

Private lenders frequently add:

- Origination fees (1–5% of the loan amount)

- Early repayment penalties

- Late payment fees that can exceed 10% of the overdue balance

- Mandatory insurance or valuation costs

These hidden charges can push the effective cost far beyond the advertised rate.

Short repayment terms

Most private loans must be repaid within 6–24 months. Borrowers who cannot refinance or repay on time face asset seizure or legal action. In the U.S., hard money lenders often secure loans with property deeds, meaning a single missed payment can trigger foreclosure.

3. When the Solution Becomes the Problem

Private capital loans are designed for short‑term use. But many borrowers use them to cover long‑term needs—medical bills, business expansion, or debt consolidation—creating a cycle of dependency.

Case study: U.S. borrower

A small business owner in Texas borrowed $100,000 from a private lender at 24% APR to cover inventory costs. After 12 months, he owed $124,000 plus $6,000 in fees. Unable to refinance, he lost his warehouse used as collateral.

Case study: EU borrower

In Spain, a homeowner took a €50,000 private loan at 18% APR to pay off credit cards. The lender added a 4% origination fee and required a notary fee of €1,200. When payments fell behind, the lender initiated foreclosure proceedings under a clause later deemed abusive by the court.

4. Legal and Regulatory Differences: U.S. vs. EU

| Region | Regulation | Common Issues | Consumer Protection |

|---|---|---|---|

| United States | Fragmented—varies by state. Some states cap interest rates; others allow up to 36% APR. | Predatory lending, asset seizure, lack of transparency. | CFPB (Consumer Financial Protection Bureau) investigates unfair practices; state laws vary. |

| European Union | Governed by national laws and EU directives (e.g., Directive 2008/48/EC on consumer credit). | Hidden fees, abusive clauses, cross‑border lenders exploiting loopholes. | National consumer agencies and EU courts enforce transparency and fairness. |

In both regions, regulatory gaps allow private lenders to operate with limited oversight. Borrowers often sign contracts without understanding the full cost or legal implications.

5. Recognizing the Warning Signs

Before accepting a private capital loan, watch for these red flags:

- No clear APR disclosure — lenders quoting “monthly interest” instead of annual cost.

- Pressure to sign quickly — urgency is a tactic to bypass due diligence.

- Collateral‑heavy terms — property or vehicle used as security for small loans.

- Unregistered lender — always verify registration with the relevant authority.

- Complex or vague contract language — hidden clauses often conceal penalties.

Transparency is the borrower’s best defense. If a lender refuses to provide full documentation, walk away.

6. The Real Cost: When You Can’t Pay

Defaulting on a private loan can have severe consequences:

- Asset loss: Collateral is seized quickly, often without court intervention.

- Credit damage: Defaults are reported to credit bureaus, limiting future access to bank loans.

- Legal fees: Borrowers may face lawsuits for unpaid balances.

- Emotional stress: Constant pressure from collection agencies and threats of foreclosure.

In the EU, courts have increasingly sided with consumers in cases involving abusive clauses—especially when lenders failed to disclose total costs. In Spain, Italy, and France, rulings under the EU Directive 93/13/CEE have forced lenders to refund excessive interest and cancel unfair penalties.

In the U.S., the CFPB and state attorneys general have prosecuted lenders for predatory practices, but enforcement remains inconsistent.

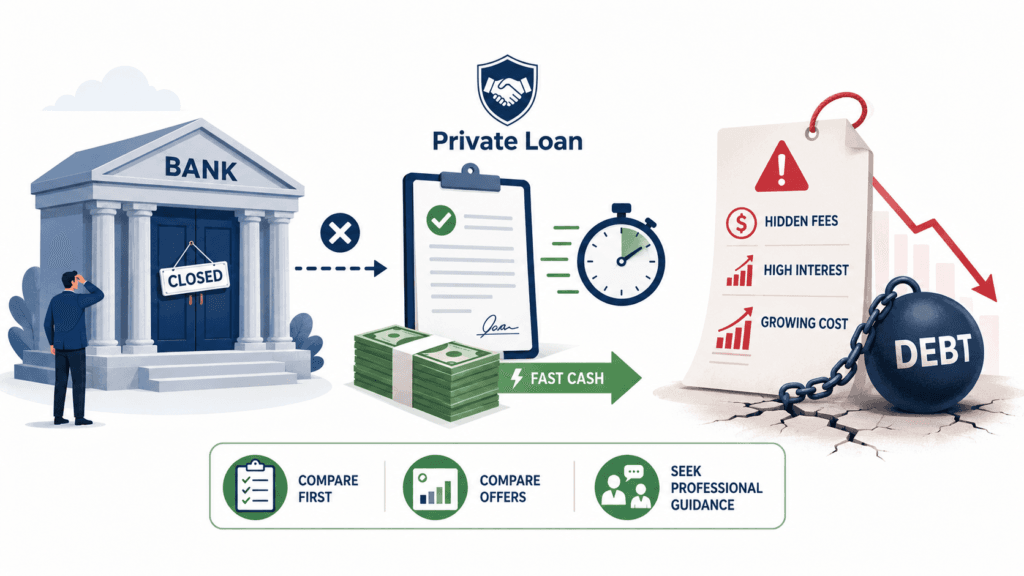

7. Real Solutions for Borrowers

1. Negotiate or refinance

If you already have a private loan:

- Ask for an extended repayment term.

- Seek refinancing through a credit union or community bank.

- Avoid rolling over the loan—this compounds interest.

2. Seek professional advice

Consult:

- A licensed financial advisor for restructuring options.

- A consumer rights attorney if you suspect abusive clauses.

- A nonprofit credit counseling agency for free guidance.

3. Report abusive lenders

- In the U.S.: file a complaint with the Consumer Financial Protection Bureau (CFPB).

- In the EU: contact your national consumer protection agency or the European Consumer Centre (ECC).

4. Consider safer alternatives

- Credit unions — lower rates, community‑based lending.

- Peer‑to‑peer lending platforms — regulated and transparent.

- Government‑backed microloans — available for small businesses and individuals.

- Debt consolidation through regulated banks — often cheaper and safer.

8. The Future of Private Lending

In 2026, private capital lending continues to grow as banks tighten credit standards. The global private debt market surpassed $1.6 trillion, according to the International Monetary Fund. While this expansion offers flexibility, it also increases the risk of predatory lending and financial instability among vulnerable borrowers.

Regulators in both the U.S. and EU are pushing for stricter disclosure rules:

- Mandatory APR transparency.

- Limits on collateral seizure.

- Standardized consumer protection frameworks across borders.

Until those reforms are universal, borrowers must rely on education, caution, and professional advice to avoid falling into the fast‑money trap.

9. Conclusion

Private capital loans can be a lifeline when banks close their doors—but they come at a steep price. What begins as a quick fix can evolve into a long‑term financial burden, especially when hidden fees and high interest rates compound over time.

The smartest borrowers in 2026 are those who treat private financing as a last resort, not a first option. By understanding the risks, comparing offers, and seeking professional guidance, you can protect yourself from the hidden cost of fast money.

Disclaimer

This article is for informational and educational purposes only. It does not constitute financial, legal, tax, credit, or consumer protection advice. Loan terms, fees, APRs, disclosures, borrower rights, and lender requirements vary by lender, state, country, credit profile, income, loan amount, and underwriting criteria. Before accepting any loan, review the full agreement, verify the lender’s legitimacy, and consider consulting a licensed financial professional or attorney.

Make sure you read this article

Microloans and Payday Credit: How to Escape the Fast-Cash Trap Legally and Safely