Lenders advertise rate ranges. They show you a floor — sometimes as low as 5.96% — and a ceiling that can reach 35.99%. What they rarely show is the internal tier system that determines exactly where you land within that range, and how dramatic the financial consequences of each tier boundary truly are.

Understanding the credit score stratification behind personal loan pricing in 2026 is not a minor optimization. For the average borrower, it is the difference between paying $2,400 or $9,000 in interest on the same loan amount.

The Five-Tier Pricing Architecture

Personal loan lenders in the United States use credit score tiers to assign interest rates. While exact tier boundaries vary by lender, the industry broadly clusters around five bands:

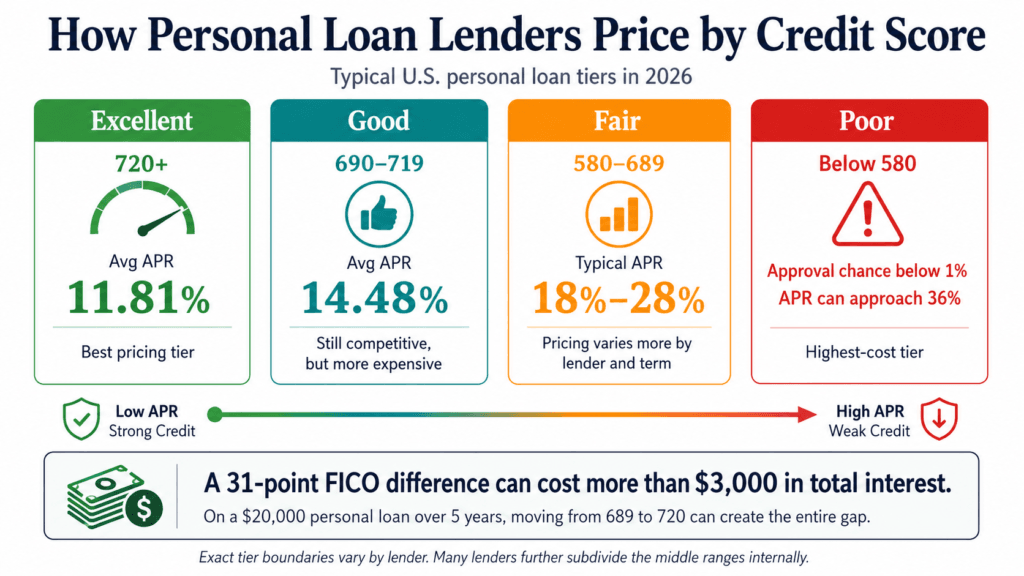

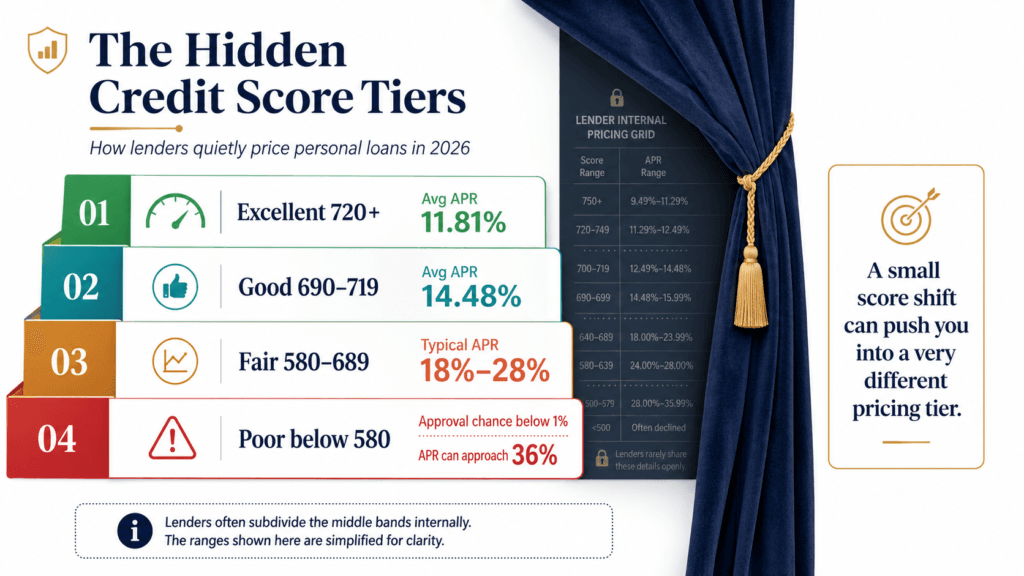

Excellent (720+): Borrowers with excellent credit (720 or higher scores) received an average rate of 11.81%, according to aggregate data from users who pre-qualified for a personal loan through NerdWallet.

Good (690–719): NerdWallet users with good credit scores (690 to 719) received an average rate of 14.48%.

Fair (580–689): Rates typically range from 18% to 28%, depending on the lender and loan term.

Poor (below 580): Borrowers with poor credit (FICO scores below 580) have a less than 1% chance of being approved for a loan at all. Those who do qualify often face APRs approaching the regulatory ceiling of 36%.

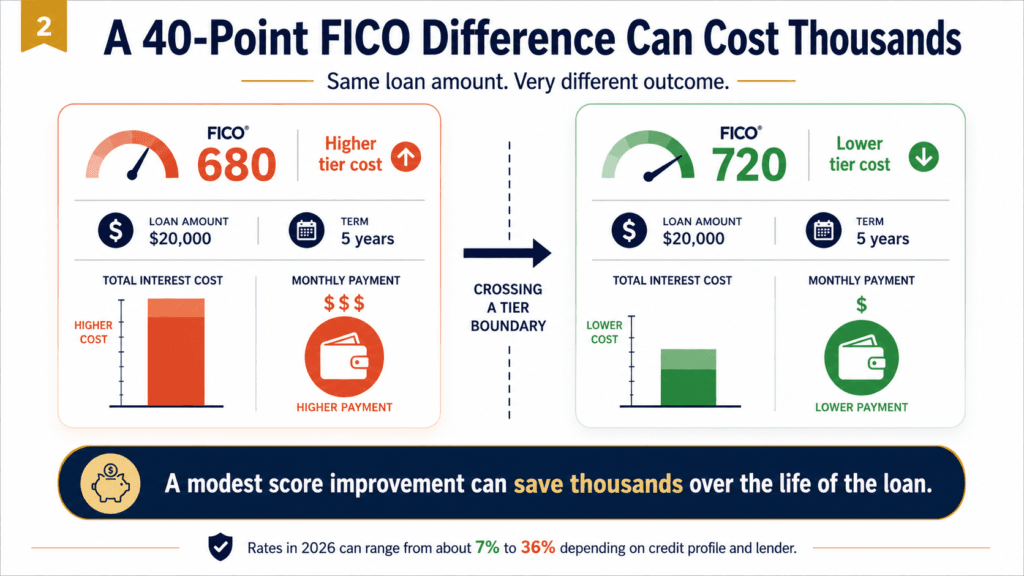

The rate differential between an excellent-credit borrower and a good-credit borrower on a $20,000 five-year loan exceeds $3,000 in total interest paid. A 31-point FICO score difference — from 689 to 720 — can represent that entire cost gap.

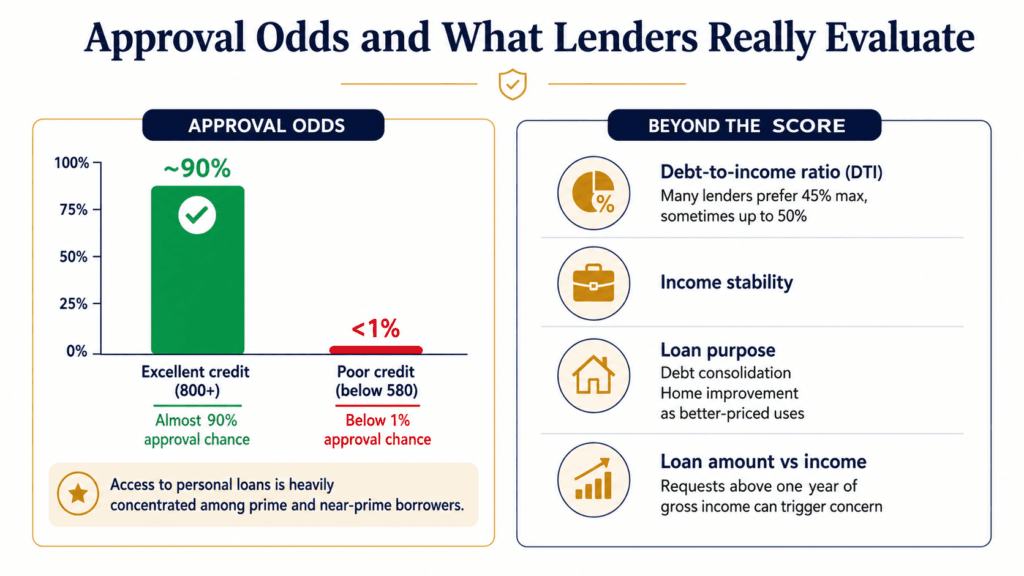

The Approval Rate Asymmetry

The impact of credit scores goes beyond pricing. Borrowers with excellent credit scores (800 FICO and above) have an almost 90% chance of being approved for a loan. Borrowers with poor credit (FICO scores below 580) have a less than 1% chance of approval.

This creates a near-impenetrable access barrier for a significant segment of the American population. The personal loan market, despite its reputation for accessibility compared to traditional bank lending, is in practice a market dominated by prime and near-prime borrowers. Subprime borrowers who do access it face origination fees of up to 12% on top of rates that can reach 36%.

What Lenders Actually Evaluate Beyond the Score

Credit score is the primary variable, but it is not the only one. Lenders in 2026 increasingly run multi-factor underwriting models that weight:

Debt-to-income ratio (DTI): Conventional lenders prefer a maximum DTI ratio of 45%, but may allow up to 50% for borrowers with higher credit scores and additional reserves.

Income stability: Self-employed borrowers, or those with gaps in employment history, typically face stricter scrutiny regardless of credit score.

Loan purpose: Average interest rates vary across different loan purposes. Debt consolidation loans and home improvement loans typically command better pricing than loans for undefined personal use.

Loan amount relative to income: Requesting a loan amount that represents more than one year of gross income is a red flag in most automated underwriting systems.

The Pre-Application Credit Repair Window

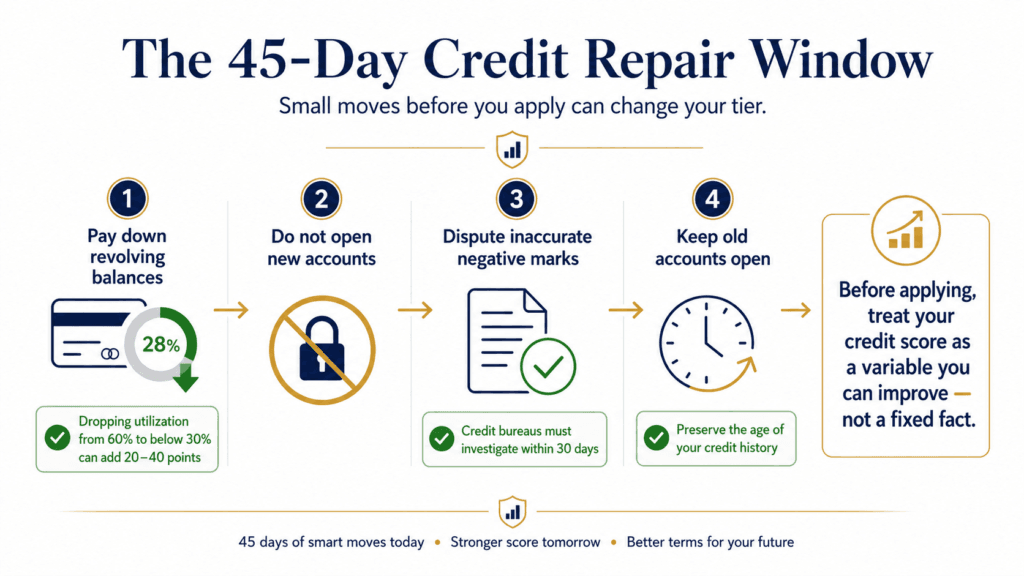

Most borrowers approach lenders with the credit profile they currently have, without recognizing that a 45-day preparation period can meaningfully shift their tier placement. The actions that produce the fastest measurable credit score improvements are:

Pay down revolving balances. Credit utilization — the ratio of credit card balances to credit limits — is the second most influential factor in FICO scoring, after payment history. Reducing utilization from 60% to below 30% can add 20 to 40 points in a single billing cycle.

Do not open new accounts before applying. Each new credit account temporarily lowers the average age of your credit history and generates a hard inquiry.

Dispute inaccurate derogatory marks. The credit bureaus — Experian, Equifax, and TransUnion — are legally required to investigate disputes within 30 days under the Fair Credit Reporting Act. Errors on credit reports are more common than most consumers realize.

Avoid closing old accounts. Closed accounts shorten your average credit history length, which can lower your score even when the account had a positive payment record.

The Bottom Line

Overall, personal loan interest rates in 2026 range from around 7% to 36% depending on the borrower’s credit profile and the lender. The 29-percentage-point spread between the floor and the ceiling of that range is not arbitrary — it maps almost entirely onto the five credit score tiers that lenders use internally.

Before applying for any personal loan, treat your credit score not as a fixed fact but as a variable you can influence. Even a modest improvement — achieved in 30 to 45 days — can move you across a tier boundary and represent thousands of dollars in savings over the life of a loan.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Rates, fees, and data referenced are based on publicly available sources as of May 2026 and are subject to change. Always consult a licensed financial professional before making any borrowing decision.

Sources

- NerdWallet. (May 2026). Average Personal Loan Interest Rates for May 2026. nerdwallet.com

- Credible. (April 2026). Personal Loan Statistics, Trends, and Demographics in 2026. credible.com

- LendingTree. (December 2025). Minimum Mortgage Requirements for 2026. lendingtree.com

- WalletHub. (Q1 2026). Average Personal Loan Interest Rates for 2026. wallethub.com

- Fannie Mae. (April 1, 2026). Eligibility Matrix. fanniemae.com

- Consumer Financial Protection Bureau (CFPB). How to Improve Your Credit Score. consumerfinance.gov

- Experian. What Is a FICO Score? experian.com