When you apply for a mortgage, you probably picture a loan officer leaning back in a chair, reading your file and weighing your character. That’s not what happens. Within seconds of your application hitting the system, a piece of software has already reached a verdict — approve, refer, or decline — and the person you’re talking to is mostly there to gather documents and confirm what the algorithm decided. In 2024, lenders turned down close to one in five home-loan applications. The good news: this gatekeeper isn’t a mood or a hunch. It’s a model with rules — and rules can be understood, prepared for, and, when the answer is no, answered.

This article is educational and is not financial or legal advice. Loan rules, rates, and guidelines vary by lender and change over time. See the full disclaimer at the end.

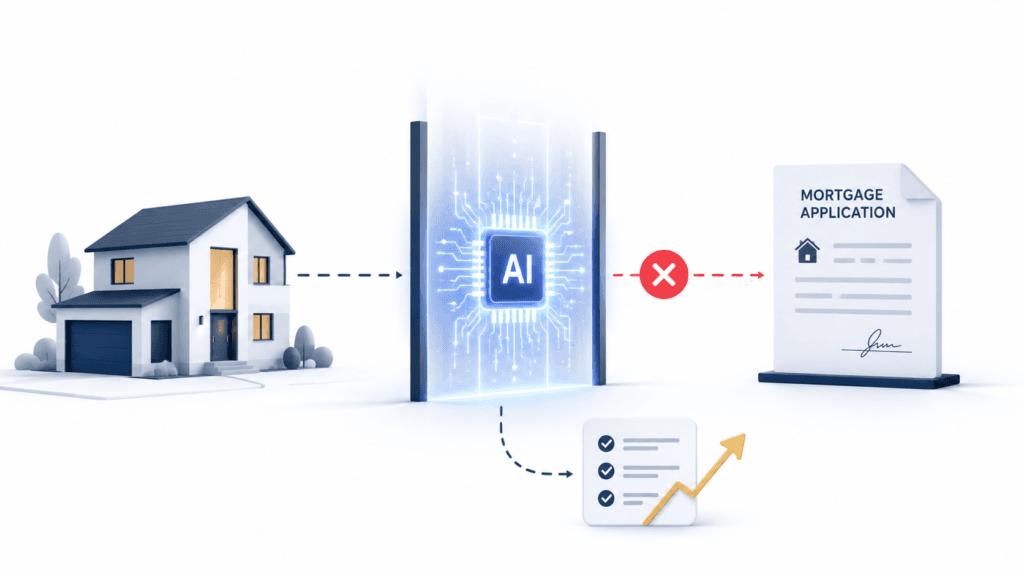

Meet the gatekeeper

The software that actually decides your mortgage

Behind most U.S. home loans sit two automated underwriting systems: Fannie Mae’s Desktop Underwriter (DU) and Freddie Mac’s Loan Product Advisor (LPA). FHA loans run through the same engines using a tool called the TOTAL Scorecard. You hand over your numbers, and the system returns a recommendation almost instantly — for DU, a result like “Approve/Eligible” or “Refer”; for LPA, “Accept” or “Caution.” A human underwriter still verifies your documents and can override the machine in either direction, but the algorithm sets the path your file travels.

It feels impersonal because it is. But impersonal cuts both ways: the system doesn’t get tired, annoyed, or suspicious. It weighs the same factors for everyone, in the same order, every time. Once you know what it’s looking at, you stop guessing and start preparing.

What it weighs

The four C’s, and the numbers behind them

Strip the system to its core and it’s scoring four things lenders have weighed for a century — the “four C’s.” Each one is a place you can win or lose before you ever speak to a person.

Credit. Your score still guards the front door. Conventional loans generally want about 620; FHA opens at 580 with 3.5% down, or as low as 500 with 10% down. VA and USDA loans set no government minimum, but individual lenders add their own overlays, often in the 580–640 range.

Capacity. This is your debt-to-income (DTI) ratio — the share of your gross monthly income already committed to debt — and it’s the single most common reason applications get denied. Here the data overturns a popular myth. The famous “43% limit” isn’t the wall most people think: the Consumer Financial Protection Bureau replaced that ratio-based rule with a price-based standard back in 2021. A St. Louis Fed analysis of more than 30 million applications found lenders treat a 45% DTI about the same as a 35% one — but once your ratio climbs past 50%, denial rates jump 15 to 17 percentage points.

Capital. The system looks at your down payment and your cash reserves — the cushion left after closing. Put down less than 20% on a conventional loan and you’ll usually pay private mortgage insurance until you build enough equity. Thin reserves can tip a borderline file the wrong way, which is exactly why it pays to know how to build a down payment faster.

Collateral. Finally, the home itself. The loan-to-value ratio and the appraisal decide whether the property backs the loan. A low appraisal can derail an otherwise-approved borrower, and surprise costs at the table catch people off guard — so go in knowing what closing costs actually run.

A 2026 shift worth knowing

The credit-scoring machine is changing

For decades, Fannie Mae and Freddie Mac required one credit model — Classic FICO — pulled from all three bureaus. That’s now changing. After validating two newer models in 2022, the Federal Housing Finance Agency has begun letting lenders use VantageScore 4.0 alongside Classic FICO, with FICO Score 10T on the way; the agencies expect to publish historical 10T scores in the summer of 2026. The long-discussed move from a three-bureau “tri-merge” to a two-bureau report has been put on hold, so for now most files still pull all three.

Why should a borrower care? Because the newer models read your history differently. They factor in rent and utility payment history that Classic FICO ignores, and they treat paid-off medical collections more gently. If you have a thin file, a strong record of paying rent, or recently cleared medical debt, you may simply score better under the new models — and because adoption is uneven, the same file can get different scores at different lenders. It’s one more reason to shop around, and to make sure your reports are clean before you apply.

When it says no

Why the algorithm rejects you — and the fix for each

A denial almost always traces back to one of a handful of specific triggers. The Federal Reserve notes that lenders must report their reason from a standard list — debt-to-income, credit history, collateral, insufficient cash, employment history, unverifiable information, and a few others — and in practice, DTI and credit are the two that come up most. The reason matters, because each one has a different move.

| Why it said no | What it means | Your move |

|---|---|---|

| DTI too high | Your monthly debts eat too much of your income — especially over ~50%. | Pay down balances and avoid new debt; clear high-interest cards and recheck your DTI before reapplying. |

| Credit too low or thin | Your score is under the cutoff, or your file is too sparse to score well. | Build your score, hit the target for your loan, and ask about VantageScore 4.0. |

| Not enough cash | Down payment or reserves fall short of the program’s minimum. | Save faster or tap down-payment assistance programs. |

| Loan amount too large | You’re above the 2026 conforming limit of $832,750, into jumbo territory. | Borrow less, put more down, or learn how jumbo loans work. |

| Wrong loan for you | You don’t fit conventional rules but might fit a government-backed loan. | Compare FHA, VA, and conventional, or zero-down USDA and VA options. |

| Property or appraisal | The home appraised low or has condition or title issues. | Renegotiate the price, dispute the appraisal, or change the property. |

The cheat sheet

Match yourself to the right loan

Half of beating the gatekeeper is applying for the loan you actually fit. A score or down payment that’s a “no” for one program is a comfortable “yes” for another.

| Loan type | Typical min. score | Min. down payment | Best for |

|---|---|---|---|

| Conventional | ~620 | 3%–5% (20% to skip PMI) | Solid credit and steady income |

| FHA | 580 (or 500 with 10% down) | 3.5% | Lower credit or smaller savings |

| VA | No federal minimum (~580 overlay) | 0% | Eligible veterans and service members |

| USDA | No federal minimum (~640 overlay) | 0% | Eligible rural and lower-income buyers |

Turning a no into a yes

What to do when the answer is “Refer” — or “Decline”

If the engine returns a “Refer,” your file isn’t dead; it’s going to a person. A human underwriter can weigh compensating factors the algorithm undervalues — big reserves, a long stable job, a low loan-to-value ratio — and FHA and VA loans expressly allow manual underwriting for exactly these cases. If you get a flat decline, you still have moves:

- Shop more lenders. Overlays and credit models vary, so a “no” at one lender can be a “yes” at the next — especially one running the newer scoring models. While you’re at it, learn how to negotiate a lower rate.

- Try a portfolio lender or credit union. Loans they keep in-house aren’t bound by Fannie/Freddie rules and can use more personal judgment.

- Bring more down, or add a co-borrower to strengthen capital and capacity at once.

- Rethink the product. An adjustable-rate loan or a different program may change the math, and avoiding common first-time buyer mistakes keeps your next application clean.

The bottom line

The invisible gatekeeper can feel cold and final, but it’s neither. It’s a model — predictable by design — and predictability is a gift, because it means the path to “yes” is knowable. Get your DTI under that 50% cliff, push your score past your loan’s cutoff, bring enough cash, fix what’s wrong on your reports, and apply for the program you actually fit. Then, if the software still hesitates, remember a “Refer” is an invitation to a human, not a closed door.

A mortgage denial is rarely a “no.”

Far more often, it’s a “not yet.”

And the moment you do get in, the same discipline keeps paying off — it’s what lets you later refinance into a better rate or pay your mortgage off years early. The gatekeeper decides whether you get in the door. What you do next is entirely yours.