Disclaimer

This article is for informational and educational purposes only. It does not constitute legal, financial, or immigration advice. SBA policies, federal regulations, and lending requirements can change rapidly. Always consult a licensed business attorney, a certified financial advisor, and a qualified immigration professional before making decisions that affect your business or immigration status.

Imagine spending years building something real — a business with employees, a payroll that hits every two weeks, a tax return that shows up on time, a community that depends on what you created. You did everything right. You followed the rules, obtained your green card, established your credit, and built a plan that included growing your business through an SBA-backed loan.

Then, in a matter of weeks, that plan became illegal — not because anything about your business changed, but because a federal policy shift erased your eligibility overnight.

This is the reality that hundreds of thousands of lawful permanent residents are now navigating. If you own a business as a green card holder, this guide is designed to give you the clearest, most complete picture of what changed, why it matters, and — most importantly — what your real options are right now.

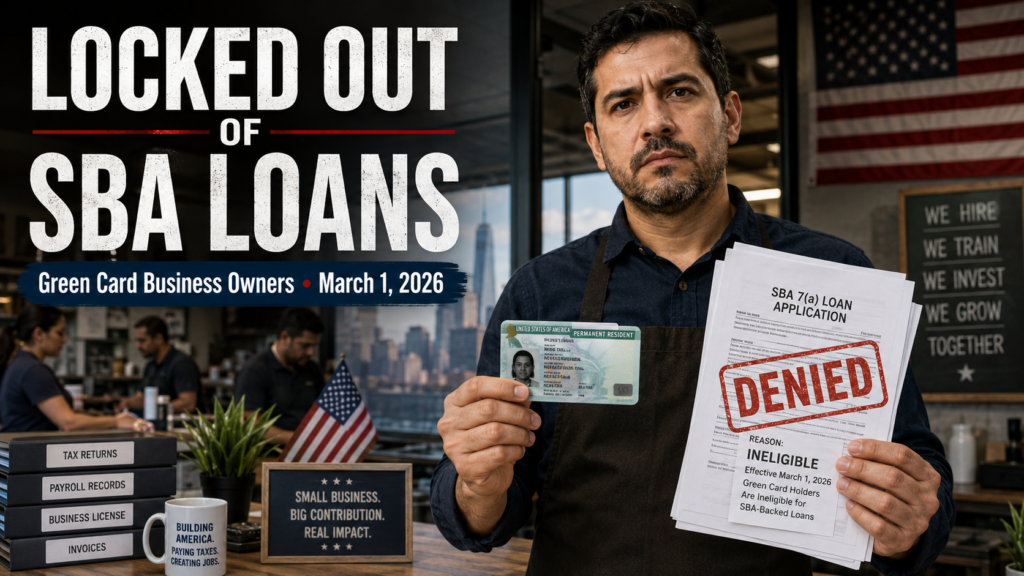

Infographic — The Rule That Changed Everything

Source: SBA Policy Notice, February 2, 2026 | Effective date: March 1, 2026

What Actually Changed — And Why You Should Care

First, let’s be absolutely clear about what an SBA loan actually is — because a lot of people hear “SBA” and assume it’s some kind of government handout or grant. It is neither.

The Small Business Administration is a federal agency whose core lending function is to guarantee a portion of loans made by private banks and credit unions. That guarantee — typically 75% to 85% of the loan value — reduces the risk for the lender, which allows them to offer terms that the open market would never produce: longer repayment windows (up to 25 years for real estate), lower down payments (as little as 10%), and interest rates that track the prime rate rather than the riskier commercial lending market.

For small business owners without inherited capital, industry connections, or Ivy League alumni networks, SBA loans have been the primary mechanism for accessing real growth capital. The program has financed hospitals, restaurants, manufacturing facilities, tech startups, and everything in between. It is, in practical terms, the cornerstone of small business financing in America.

For decades, the eligibility rule was clear: at least 51% of the ownership of a business applying for an SBA loan needed to be held by U.S. citizens or lawful permanent residents. Green card holders counted. They went through years of legal immigration processes, extensive background checks, and government vetting to earn that status — and the SBA recognized that status as sufficient for participation.

On February 2, 2026, the SBA published a policy notice that took effect March 1, 2026. The new rule eliminated that recognition completely. As of that date, 100% of a business’s ownership must consist of U.S. citizens or U.S. nationals. Not 51%. Not 80%. Every single percent.

That means even a business where a green card holder owns a 2% stake is now disqualified. It means indirect ownership counts — if a holding company is an applicant and one of that company’s partners holds a green card, the application is rejected. And it applies across every SBA program: 7(a) loans, 504 commercial real estate loans, Surety Bond guarantees, and even the Microloan program targeted at businesses that need $50,000 or less.

The Economic Reality Behind the Policy

To understand why this policy has generated such widespread alarm across lending institutions, business advocacy groups, and state governments, you have to look at the numbers — the real economic data behind immigrant entrepreneurship in the United States.

| Metric | Data Point | Source |

|---|---|---|

| Lawful permanent residents in the U.S. | ~14 million | DHS Office of Immigration Statistics, 2024 |

| Immigrant-owned businesses in California (share of total) | ~40% | CA Governor’s Office of Business & Economic Development |

| Income generated by immigrant-owned businesses in CA (2023) | $28.4 billion | CA Governor’s Office of Business & Economic Development |

| Estimated share of national SBA loan portfolios with LPR ownership | 5–15% | Mortgage Bankers Association estimate, 2026 |

| SBA 7(a) loans approved in FY2024 | 70,000+ | SBA Annual Report FY2024 |

| Total SBA 7(a) loan volume in FY2024 | $31.1 billion | SBA Annual Report FY2024 |

The Mortgage Bankers Association, along with dozens of state and national chambers of commerce, has raised formal objections to the policy. Small Business Majority organized a coalition letter describing the rule as “a misguided approach that ignores critical economic data underscoring the job-creating power of the immigrant community.” Senators including Ed Markey and Representatives including Nydia Velázquez introduced the Investing in the American Dream Act specifically to restore the previous 51% ownership threshold.

None of that has changed the policy yet. Which is why the focus for affected business owners has to be on what is available right now, not on what might change if legislation eventually moves.

Infographic — SBA Programs Now Closed to Green Card Holders

All four major SBA programs now require 100% U.S. citizen ownership. Source: SBA Policy Notice, February 2, 2026.

Your Real Financing Alternatives — A Detailed Guide

Here is the most important thing to understand: losing SBA access is not losing access to capital. It is losing access to the easiest, most familiar capital. Those are very different problems. One shuts the door entirely. The other requires you to learn where the other doors are — and most affected business owners genuinely don’t know yet.

Let’s go through every legitimate alternative in detail.

Alternative #1: Community Development Financial Institutions (CDFIs)

This is the single most important alternative that most affected business owners have not yet fully explored — and it should be the first call you make.

CDFIs are Treasury-certified lenders — often nonprofits or mission-driven financial institutions — that exist specifically to provide capital access to businesses that are underserved by conventional banking. They were created precisely for situations like this. Many have been serving immigrant entrepreneurs long before this policy change happened.

What makes CDFIs structurally different from traditional banks:

- No citizenship requirement. CDFIs are not bound by SBA rules. Your immigration status — as long as you are legally present in the United States — is generally not a disqualifying factor.

- Alternative credit evaluation. Many CDFIs accept ITIN numbers in addition to Social Security numbers and use holistic underwriting that weighs your cash flow, business history, and community impact rather than just a FICO score.

- Real loan sizes. This is not just microloans. Accion Opportunity Fund, for example, offers loans up to $250,000. Some CDFIs with real estate programs can go higher. DreamSpring serves businesses across the Southwest with similar capacity.

- Technical assistance. Many CDFIs pair their lending with free business coaching and financial counseling — something traditional banks don’t offer.

How to find a CDFI near you: Go directly to the U.S. Treasury Department’s CDFI Fund website at cdfifund.gov and use the award database or certified institution list filtered by your state. Do not just fill out an online form — call the organization directly, explain your situation, and ask specifically whether they have programs for immigrant-owned businesses. Many do, and some have set up dedicated programs since the SBA policy change.

You can also read our article on government loan programs and assistance available in 2026, which covers several overlapping financing mechanisms.

Alternative #2: Conventional Bank and Credit Union Business Loans

Traditional business loans from banks and credit unions remain fully available to lawful permanent residents. The federal SBA policy change affects SBA-backed products only — it has no bearing on private lending decisions made by commercial banks, community banks, or credit unions using their own capital and risk assessment frameworks.

The honest trade-off: conventional business loans are harder to qualify for and more expensive than SBA-backed products. Here is what lenders typically look for:

| Factor | SBA Loan (Was) | Conventional Business Loan |

|---|---|---|

| Minimum Credit Score | 620–640 | 680–720+ |

| Down Payment | 10% | 20–30% |

| Time in Business | 2+ years typical | 2–3 years required |

| Interest Rate Range | Prime + 2.25–4.75% | Prime + 3–6% |

| Max Loan Term | 25 years (real estate) | 10–20 years |

| Citizenship Requirement | 100% U.S. citizen (new) | None — LPRs fully eligible |

Credit unions deserve particular attention here. Unlike commercial banks that are accountable to shareholders, credit unions are member-owned cooperatives that operate with a mission focus on serving their members — not maximizing profit margins. They frequently offer more favorable terms on business loans, especially for established members with a solid banking relationship. If you don’t already belong to a credit union, joining one and establishing a relationship now — before you need the loan — is one of the most concrete steps you can take.

For context on how your credit profile affects your access to financing generally, see our guide on how to improve your credit score before applying for financing — many of the same principles apply to business credit.

Alternative #3: State-Level Small Business Loan Guarantee Programs

Several state governments have moved quickly to create or expand programs that partially replicate the SBA guarantee structure — without the federal citizenship requirement. These programs are especially important for business owners in high-immigrant-population states where lawmakers have recognized the economic stakes of losing entrepreneurial capital.

| State | Program | Key Features | Where to Apply |

|---|---|---|---|

| California | IBank Small Business Finance Center | Loan guarantee up to $50M, no federal citizenship requirement, disaster and small biz programs | ibank.ca.gov |

| New York | Empire State Development Small Business Programs | Linked deposit loans, Excelsior linked deposit, immigrant-owned business support | esd.ny.gov |

| Texas | Texas Economic Development and Tourism — Capital Programs | Small business loan guarantee, multiple CDFI partners statewide | gov.texas.gov/business |

| Illinois | DCEO Illinois Small Business Assistance | EDGE tax credits, small business development centers, minority biz loans | illinois.gov/dceo |

Even if you are not in one of these states, your state’s Small Business Development Center (SBDC) — a federally funded resource available in every state — can help you identify local alternatives. Find your nearest SBDC at americassbdc.org. The consultation is always free.

Alternative #4: Invoice Factoring and Revenue-Based Financing

If your business has consistent B2B revenue or predictable invoicing — think contractors, staffing agencies, service businesses, wholesale distributors, healthcare providers — invoice factoring can unlock cash flow without requiring a traditional loan approval process at all.

Here is how it works: instead of waiting 30, 60, or 90 days for your clients to pay their invoices, a factoring company advances you 80–95% of the invoice value immediately. When your client pays, the factor takes its fee (typically 1–5% of the invoice value, depending on the size and the risk profile of your clients) and forwards you the remainder.

Revenue-based financing (RBF) works differently: instead of a loan with fixed payments, the lender advances capital that is repaid as a percentage of your monthly revenue — typically 6–12% of monthly receipts — until the advance plus a factor fee is repaid. There are no fixed monthly payments and no traditional collateral requirements. RBF is most suitable for businesses with predictable, recurring revenue — software companies, subscription-based services, retail businesses with steady card volume.

Neither of these products requires citizenship verification. They are financing structures built around your revenue, not your immigration paperwork.

Alternative #5: Seller Financing for Business Acquisitions

If you were planning to acquire an existing business — a transaction that would previously have required an SBA 7(a) loan to bridge the gap between your down payment and the purchase price — seller financing is now the most viable non-bank alternative for large acquisitions.

In a seller-financed deal, the selling owner carries a portion of the purchase price through a promissory note. You pay them directly — typically over 3–7 years at an agreed interest rate — rather than going through a bank. The seller benefits from a higher sale price (they can charge a premium for the financing convenience), monthly cash flow during the note term, and often favorable capital gains tax treatment. You benefit from access to capital without a bank intermediary and without citizenship eligibility requirements.

In the current environment, where business buyers who would have used SBA financing have been sidelined, motivated sellers have genuine reason to consider seller financing. This is a negotiation conversation worth having with any seller you approach.

Infographic — Comparing Your Financing Alternatives

Rate ranges are estimates based on 2026 market conditions. Actual terms vary by lender, credit profile, and loan structure. Always compare multiple offers.

What to Absolutely Avoid: The Predatory Financing Trap

When a major financing channel closes, predatory lenders move in almost immediately. They already have. If you are a lawful permanent resident business owner who lost SBA eligibility, you are already on marketing lists being targeted by some of the most destructive financial products in the lending industry.

The product to be most wary of is the merchant cash advance (MCA). Here is how it works, and why it is so dangerous:

- Structure: The MCA company advances you a lump sum against your future credit card or bank sales. In return, they take a daily percentage of your bank deposits or card transactions — typically 10–30% — until the advance is repaid.

- True cost: MCA products do not use APR — by design. When converted to APR, effective annual rates frequently fall between 60% and 200%. Some exceed that.

- The trap: Because repayment is tied to revenue, a slow month doesn’t reduce pressure — it just extends the repayment period. Many business owners who take one MCA take a second to cover the daily withdrawals from the first. This cycle has destroyed otherwise viable businesses.

- The pitch: Fast approval (24–48 hours), no credit check, no collateral, no citizenship requirement. If someone is offering you capital this quickly with no traditional underwriting, ask yourself why.

⚠ Red Flags to Watch For

If someone contacts you offering fast business capital, calls it a “revenue advance” instead of a loan, won’t give you the APR, is rushing you toward a decision, or tells you this offer expires in 24 hours — that is a merchant cash advance or equivalent high-cost product. Walk away. Contact a CDFI or your local SBDC instead.

Your Action Plan: What to Do Starting This Week

Knowing the landscape is only useful if it leads to concrete action. Here is a week-by-week framework for green card holder business owners navigating this transition.

Week 1 — Assess and Organize

- Pull your personal and business credit reports from annualcreditreport.com (free, federally mandated)

- Compile your last 3 years of business tax returns, P&L statements, and balance sheets

- Document your business structure, ownership percentages, and any holding company arrangements

- Identify exactly how much capital you need and what it will be used for — lenders want specificity

Week 2 — Find Your CDFI and SBDC

- Visit cdfifund.gov and identify 2–3 CDFIs operating in your state

- Call each one — do not just submit an online form — and ask specifically about immigrant business owner programs

- Schedule a free appointment at your nearest SBDC (americassbdc.org) — they provide free advisory services and often know local lenders that are not widely advertised

- Check your state’s economic development agency website for state-level guarantee programs

Week 3 — Start Bank and Credit Union Conversations

- Contact your existing business bank about conventional business loan options

- Identify and join a credit union if you haven’t already — many have business lending programs

- Talk to a commercial banker at a community bank — they often have more flexibility than large national institutions

Ongoing — Document and Advocate

- Contact your congressional representatives — the Investing in the American Dream Act needs co-sponsors and public pressure

- Connect with Small Business Majority and local chambers of commerce that are advocating for policy reversal

- Share your story — the human and economic impact of this policy is still not fully understood by many lawmakers

The Legal Landscape: Challenges and What to Watch

Several business advocacy organizations have raised legal challenges to the February 2026 policy change, arguing that the SBA exceeded its statutory authority in implementing a rule change of this magnitude without going through the standard notice-and-comment rulemaking process required by the Administrative Procedure Act (APA).

The argument centers on whether the SBA’s authorizing legislation — the Small Business Act itself — requires or even permits citizenship as a sole eligibility criterion. Critics point out that lawful permanent residents have historically been recognized as members of the U.S. economic community for virtually every other federal economic program and that the policy change represents a dramatic departure from decades of consistent administrative interpretation.

Whether those challenges succeed — and on what timeline — remains genuinely uncertain. What is certain is that waiting for a legal or legislative resolution before taking action on your financing needs is not a strategy. Build the alternative financing relationships now. If the policy is reversed, you will be better positioned than before. If it is not, you will have already established the capital access your business needs.

For broader context on how federal financial policy changes affect access to credit and lending markets, see our guides on how lenders evaluate your debt-to-income ratio and strategies for negotiating better loan terms.

Frequently Asked Questions

Can I add a U.S. citizen co-owner to restore SBA eligibility?

Technically yes — if 100% of the ownership, including all direct and indirect owners, consists of U.S. citizens, the business becomes SBA-eligible. But this is a significant structural and legal decision with ownership, tax, and relationship implications. Consult a business attorney before making any ownership changes specifically to meet this threshold. And remember: SBA loans are still credit-based — meeting the citizenship test does not guarantee approval.

Does this affect SBA loans that were already approved?

If your SBA loan was fully approved and funded before March 1, 2026, it is generally not affected. Existing borrowers in good standing should not see changes to their loans. However, refinancing, modifications, or additional SBA credit after March 1 would be subject to the new rule. Check with your lender if you have any active SBA products and want to understand how the change applies to your specific situation.

What if I am in the process of becoming a U.S. citizen?

Naturalization applications are not the same as citizenship. Until you have taken the Oath of Allegiance and received your Certificate of Naturalization, you are still classified as a lawful permanent resident and are subject to the new SBA restriction. There is no “pending citizenship” exception in the current policy. That said, if you are eligible and your naturalization process is nearly complete, it may be worth timing any SBA application accordingly.

Are CDFI rates significantly worse than SBA loan rates?

They are generally higher, but not dramatically so for well-qualified borrowers. SBA 7(a) loans typically carry rates of prime plus 2.25–4.75%. CDFI business loans typically carry rates of 8–18%, with the lower end available to borrowers with strong credit profiles and documented cash flow. The gap is meaningful but manageable — especially compared to merchant cash advances or other high-cost alternatives. Think of CDFI lending as the closest structural equivalent to SBA financing that remains available to lawful permanent residents.

Can DACA recipients or TPS holders get any small business financing?

DACA recipients and TPS holders were never SBA-eligible and are not directly affected by this specific policy change — they faced different restrictions. However, CDFIs remain a primary option for these communities as well. Many CDFIs explicitly serve DACA and TPS holders and accept ITIN-based applications. The SBDC network can also connect these business owners with appropriate resources in their specific states.

The Bottom Line

Cristina Foanene, who owns a glass company in California and was affected by this policy, said something that has stayed with many people who followed this story: “I felt like the SBA understood small businesses better than a big bank ever will. They want to make sure you’re not just buying a property to buy a property, but that you’ll bring a benefit to the community, create more jobs.”

That philosophy — capital tied to community impact — is exactly the framework that CDFIs also operate under. The policy change did not eliminate mission-aligned lending. It just moved it to a different set of institutions.

If you are a lawful permanent resident business owner, the most important thing you can do right now is stop waiting for the policy to change and start building the financing relationships that are available today. Call your local CDFI this week. Schedule an appointment with your SBDC. Talk to a community banker. Document your financials so you are ready to apply.

The business you built is still worth financing. The path to that financing just looks different than it did six months ago.

Related Reading on RateGlint

- Personal Loans vs. Credit Cards: Which Should You Use?

- How to Get Out of Credit Card Debt in 2026

- Emergency Fund: How Much Do You Really Need?

- Debt-to-Income Ratio: What Lenders Really Look At

- Pay Off Debt vs. Invest: The Exact Formula to Decide

Important Disclaimer

This article is published for general educational and informational purposes only. It does not constitute legal advice, financial advice, or immigration counsel. The policy information referenced reflects publicly available federal agency communications as of the article’s publication date; SBA policies, lending regulations, and program eligibility criteria are subject to change. Rates, program details, and lender requirements mentioned are for illustrative purposes and may vary significantly based on individual circumstances, location, and market conditions. Always consult a licensed attorney, certified financial advisor, and qualified immigration professional before making decisions that affect your business, finances, or immigration status. RateGlint.com does not guarantee any particular outcome from the strategies or resources described in this article.