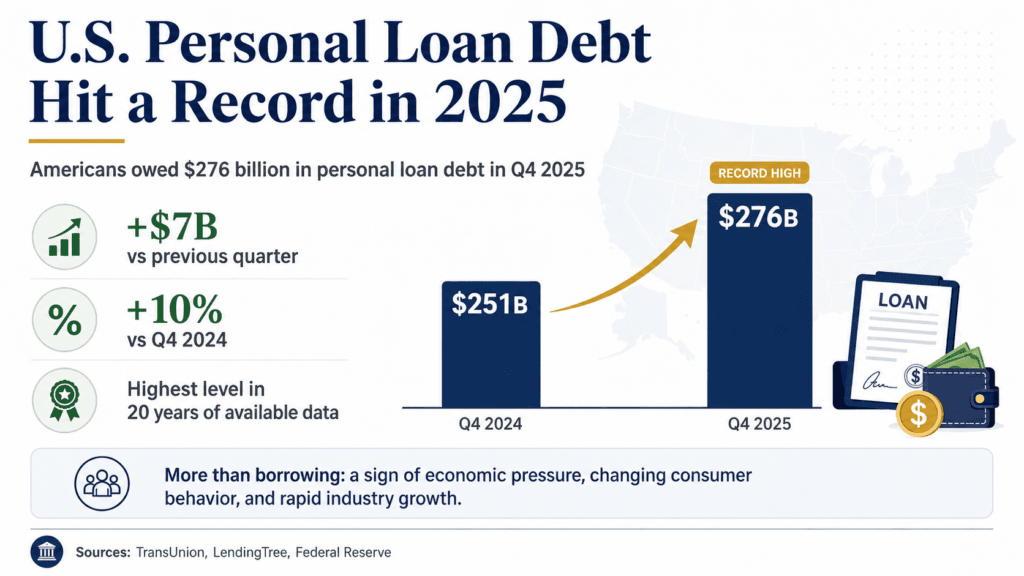

The personal loan market in the United States reached a record in 2025 that most financial news outlets barely mentioned. Americans owed $276 billion in personal loan debt as of Q4 2025 — up $7 billion from the previous quarter, marking the highest amount in the 20 years for which data is available. This represents a 10% increase from Q4 2024, when Americans owed $251 billion.

This is not simply a story about borrowing. It is a story about economic pressure, shifting financial behavior, and a personal loan industry that has grown faster in the last three years than at any point in modern history. The data, sourced from TransUnion, LendingTree, and the Federal Reserve, paints a detailed picture of who is borrowing, why, and what is likely to happen next.

26 Million Americans Now Carry a Personal Loan

As of Q4 2025, 26.4 million Americans have a personal loan, up from 24.5 million in Q4 2024. That is nearly 2 million new borrowers added to the market in a single year — a rate of adoption that reflects the combination of persistently high credit card rates and a personal loan market that has become significantly more accessible through online and fintech lenders.

The average unsecured personal loan balance is $11,699 as of Q4 2025, according to TransUnion. When borrowers open a new account, the average new balance is $6,700. Average debt per borrower peaked in Q1 2024 at $11,829, while the average new account balance peaked a year prior at $8,200. The gradual compression of new account balances suggests borrowers are becoming more conservative in their loan requests — a behavioral shift consistent with elevated interest rates and tighter household budgets.

Why Are Americans Borrowing?

More than half of borrowers — 51.4% — take out a personal loan to consolidate debt or refinance credit cards. The next-closest reason is paying everyday bills at 10.8%.

This data point is significant. The dominant use of personal loans is not discretionary spending or major purchases. It is debt management — specifically, using a lower-rate personal loan to exit higher-rate credit card debt. The average APR on new credit card offers is 23.77% as of February 2026, compared to a personal loan average of 12.27% according to Bankrate. For a borrower carrying $15,000 in credit card debt, that 11-percentage-point difference translates into thousands of dollars saved annually — which explains why debt consolidation dominates the market.

The Fintech Revolution: Who Is Winning the Personal Loan Market

Perhaps the most structurally significant shift in the personal loan market in recent years is not the volume of debt — it is who holds it. The balance of power between traditional lenders and fintech platforms has fundamentally changed.

Fintech companies now service more unsecured personal loan debt than banks and credit unions combined, according to TransUnion data. Individuals with personal loan accounts at fintech companies have the highest average outstanding balances compared to those who borrowed from other personal loan providers.

In 2025, personal loans became the largest target segment in digital lending. Personal installment loans accounted for 37.51% of the total volume of loans issued in the digital lending segment, and the same trend is expected to continue in 2026. The reason is structural: personal loans are ideally suited to digital underwriting because they are standardized products — fixed term, fixed payment schedule, and predictable documentation requirements.

Fintech lenders, once disruptors, now rival and often outperform traditional banks in speed, accessibility, and niche targeting. Platforms like LendingClub, Prosper, and SoLo Funds leverage peer-to-peer models and alternative data to serve varied borrower needs, while newer online entrants compete on APR, funding speed, and user experience. This competition pressures legacy institutions to streamline processes and reduce fees. My Spain Visa

For borrowers, this structural competition is a net positive: it drives rates down, increases access, and forces traditional banks to match the digital convenience that fintech platforms have normalized. Two out of five respondents to a U.S. Consumer Lending Satisfaction Study said lenders acted on their personal loan requests within an hour — a benchmark that would have been unthinkable a decade ago and that traditional branch-based banking still struggles to match.

Who Borrows Most — and Who Struggles Most

Baby boomers hold the most outstanding personal loan debt on average at $22,551, while Gen Z holds the least at $8,710. This generational gap reflects both the longer credit histories of older borrowers — who qualify for higher loan amounts — and the growing participation of younger Americans in a personal loan market they are accessing primarily through mobile-first fintech platforms.

Generational behavior is also diverging in how borrowers use these loans. Millennials and Gen Z skew heavily toward debt consolidation and immediate financial relief, while boomers tend to carry larger balances accumulated over longer repayment periods. According to lending data, millennials represent the largest group of digital borrowers at 36.6%, followed by Generation X at 25.8% and boomers at 20.5%.

Geographically, the data reveals sharp regional disparities that reflect broader economic inequality. Massachusetts has the highest average new personal loan account balance at $11,505. Oklahoma has the lowest average new account balance at $3,010 and the highest delinquency rate at 7.15%. These regional extremes illustrate how local economic conditions — income levels, employment stability, and cost of living — translate directly into borrowing capacity and repayment ability.

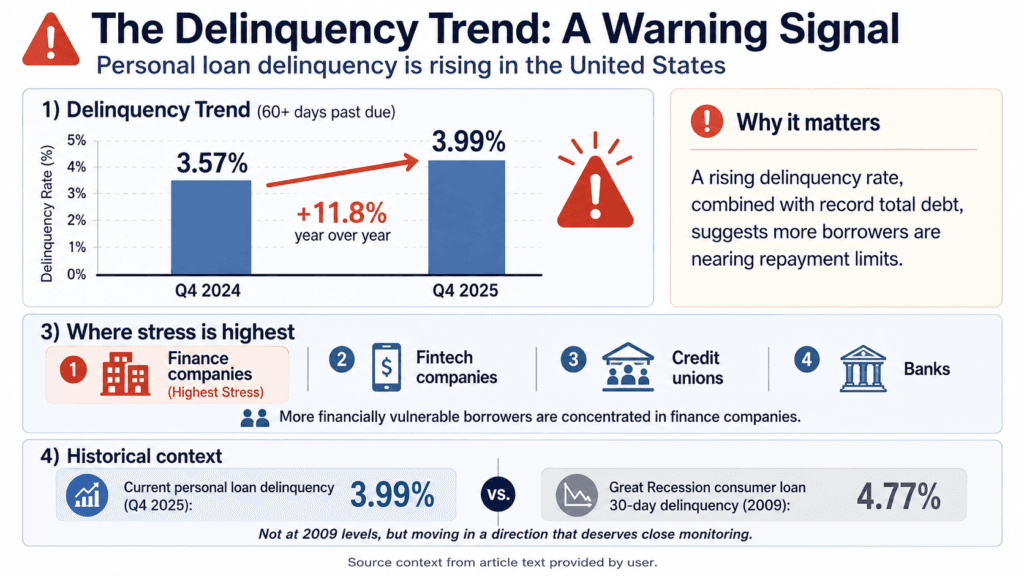

The Delinquency Trend: A Warning Signal

Delinquency — the leading stress indicator in consumer lending — is rising and deserves serious attention. The delinquency rate (60 days or more past due) for personal loans is 3.99% as of Q4 2025, up from 3.57% a year earlier.

While 3.99% may appear modest in absolute terms, the trajectory matters. A delinquency rate increasing by more than 10% in a single year, against a backdrop of record total debt, indicates that a meaningful subset of borrowers is reaching the limits of their repayment capacity. Delinquency is a more significant issue for finance companies than for other types of personal loan providers. Even though they lend smaller amounts, their rate of past due accounts is higher than fintech companies, credit unions, and banks. This suggests that the most financially vulnerable borrowers — those turning to subprime finance companies rather than banks or fintechs — are bearing a disproportionate share of the repayment stress in the current rate environment.

For context, the 30-day delinquency rate on consumer loans during the Great Recession in 2009 reached 4.77%. The current trajectory, while not yet at that threshold, is moving in a direction that warrants monitoring from both borrowers and lenders. LendingTree

The Rate Environment That Shaped This Market

Average personal loan interest rates on 3-year loans were at 13.45% APR for the week ending May 3, 2026, while 5-year loan rates averaged 17.79% APR. Rates for 3-year loans are down significantly from 14.39% at this time last year, and 5-year loan rates are down from 20.39%.

Bankrate projects an average personal loan rate of approximately 12% for 2026 — a modest decrease from where rates ended in December 2025. Their projected low of 11.8% for 2026 would represent the lowest average rate since the end of 2023, though still well above the 10.27% average seen at the end of 2021. Bankrate

The Federal Reserve’s decision to hold rates unchanged at its most recent meeting — citing persistent inflation concerns — means the personal loan rate environment will remain elevated through at least mid-2026. For borrowers, this reinforces the importance of rate shopping aggressively and prioritizing lenders with no origination fees wherever possible.

What the Data Actually Tells Us

The $276 billion figure is not a sign of reckless borrowing. The data shows a population using personal loans instrumentally — predominantly to escape higher-cost credit card debt in an environment where those card rates have reached 23.77%. The volume is high, but the purpose is largely rational.

What the data does reveal is a market under structural tension: fintech platforms displacing traditional banks, delinquency rates climbing, average balances growing, and a record number of Americans leaning on unsecured borrowing to manage their financial lives. The digitization of lending has democratized access to personal loans in ways that genuinely benefit consumers — faster approvals, more competitive rates, and broader eligibility. But it has also made high-cost borrowing more frictionless for the segment of borrowers least equipped to manage it responsibly.

A labor market softening — or a Federal Reserve pivot back to rate hikes — would translate directly into higher personal loan rates and higher default rates simultaneously. For borrowers, the strategic lesson is clear: act on consolidation opportunities before that window narrows, compare lenders by APR rather than advertised rate, and avoid the delinquency trap by borrowing only what a fixed monthly budget can genuinely sustain.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Rates, fees, and data referenced are based on publicly available sources as of May 2026 and are subject to change. Always consult a licensed financial professional before making any borrowing decision.

Sources

- LendingTree. (March 2026). Personal Loan Statistics: 2026. lendingtree.com

- TransUnion. (2026). Consumer Credit Report Q4 2025. transunion.com

- The Motley Fool. (March 2026). Personal Loan Statistics Heading Into 2026. fool.com

- Credible. (April 2026). Personal Loan Statistics, Trends, and Demographics in 2026. credible.com

- Credible. (May 2026). Personal Loan Interest Rates in 2026 (Weekly Updates). credible.com

- Bankrate. (February 2026). Personal Loan Interest Rate Forecast for 2026. bankrate.com

- Bankrate. (May 2026). Average Personal Loan Interest Rates in May 2026. bankrate.com

- Federal Reserve Board. (August 2023). FinTech-Issued Personal Loans in the U.S. federalreserve.gov

- The Financial Brand. (2023). Should More Banks Follow Fintechs into the Personal Loan Market? thefinancialbrand.com

- Electroiq. (February 2026). Digital Lending Statistics That Show Where the Market Is Headed in 2026. electroiq.com